Happy new year everyone! The start of the new year is a time to reflect on the past and look ahead to the future. 2022 was a tumultuous year for investing, with markets experiencing volatility and interest rates climbing rapidly. These factors contributed to a decline in asset prices. While the Federal Reserve’s efforts to curb inflation seem to be having some effect, there is no guarantee that the situation will improve. In fact, it is possible that interest rates may continue to rise, putting even more strain on the economy.

It is worth noting that while prices have fallen, there has not yet been a corresponding decrease in earnings. In times of uncertainty, investors and companies tend to become more conservative, focusing on cost-cutting and efficiency rather than growth. This can have a ripple effect on individuals and businesses throughout the economy, as people reduce their spending on non-essential items and industries that rely on consumer spending struggle.

For example, the housing market has been hit hard by the recent increase in interest rates. With monthly mortgage payments now much higher than they were a year ago, potential homebuyers are hesitant to make a purchase. This has led to a significant drop in home sales, which has had a knock-on effect on industries such as real estate, mortgage brokering, and home inspection. As those who work in these fields see their incomes decline, they may be forced to cut back on their own spending, which can then impact other businesses.

It is important to be aware of these potential impacts and to be prepared for any scenario. Building up your savings and making smart investment decisions are always good ideas, and the new year is a great time to review your financial goals and assess whether you are on track to achieve them.

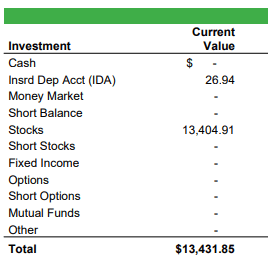

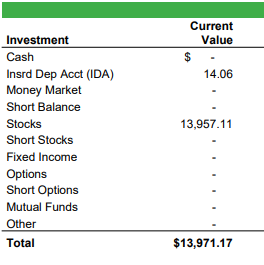

Let’s take a look at my 2022 investing results:

Q4 Performance

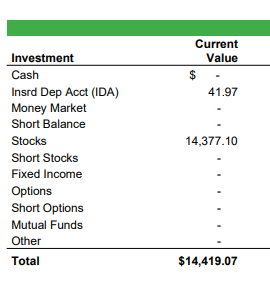

As of 1/1/2023, my 10K portfolio is worth $14,419.07. When I started on 8/19/18, the SPY had a price of $285.06 and my account started with $10,000. As of 1/1/2023 the SPY had a price of $382.43. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation

| 10K Return(1) | SPY Return(2) | Difference(1-2) | |

| 2018(8/19-12/31) | (13.95) | (13.71) | (.24) |

| 2019 | 37.33 | 32.6 | 4.73 |

| 2020 | 21.22 | 17.59 | 3.63 |

| 2021 | 38.55 | 28.43 | 10.12 |

| 2022(1/1-12/31) | (27.25) | (18.65) | (8.60) |

| Since Inception(8/19/18) | 44.19 | 44.58 | (.39) |

| CAGR | 8.72 | 8.82 | (.1) |

While my portfolio underperformed the S&P 500 in 2022, I am happy to see that it has remained relatively close to the index since its inception. Despite the challenges of investing, I am confident in the composition of my portfolio and believe that it will perform well over time. It’s important to remember that investing can be tough, and it’s important to stay humble and cautious. As Warren Buffett has pointed out, as long-term investors, we should actually be hoping for stock prices to go down so that we can buy more shares at lower prices and increase our ownership stakes in the long run.

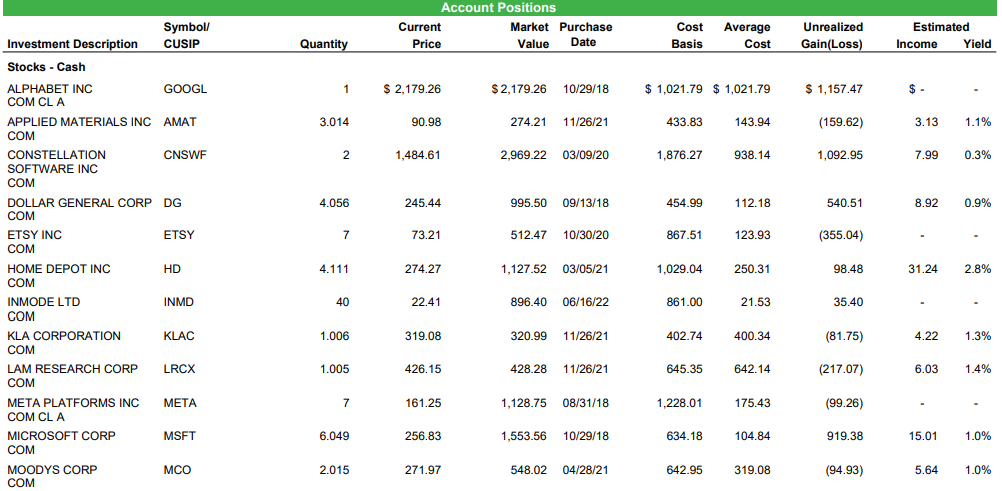

Transactions

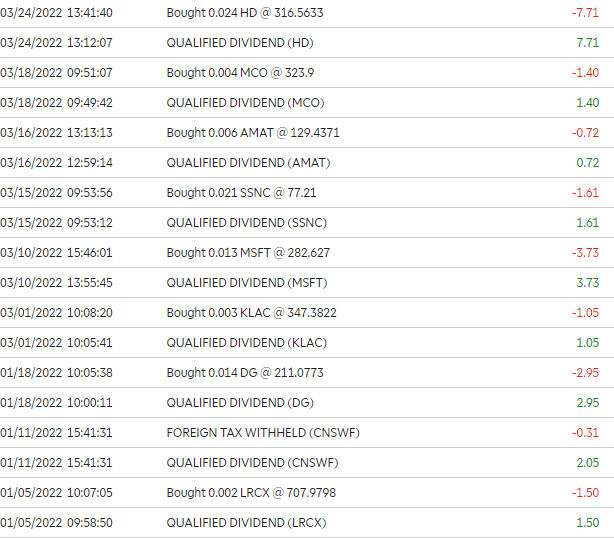

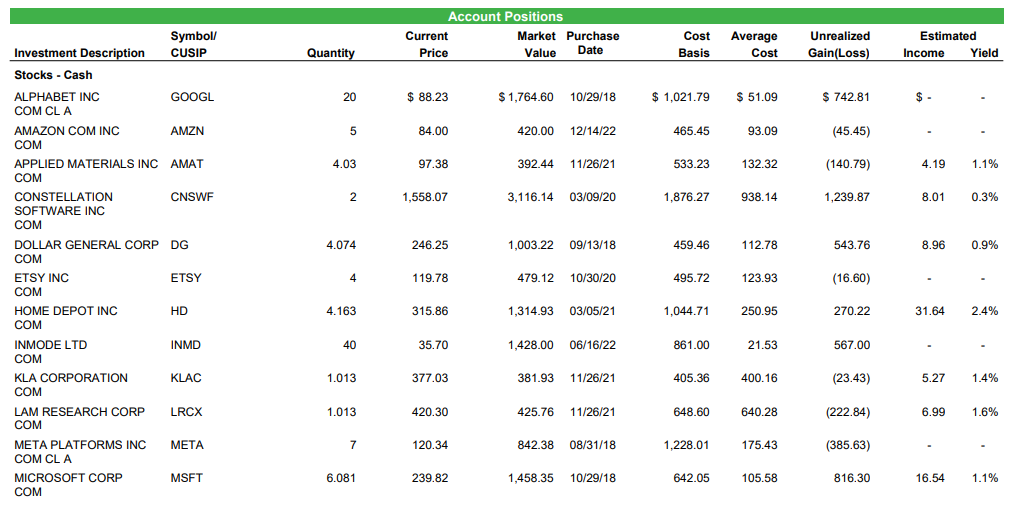

MCO- I sold my shares of Moody’s in early October. This has little to do with the long term prospects of the business, they are still top notch. They will continue dominating their corner of the market, I just thought shares were too expensive and there were better opportunities elsewhere.

ETSY- I also trimmed my Etsy position, selling off 3 of my 7 shares. I still like the company, but will admit to losing some faith. I think they operate a great business and could have robust growth in their future, but I question management capital allocation. They spent an exorbitant amount buying smaller companies like Depop and Elo7. Maybe these will be good businesses, but they paid ludicrous multiples to buy. Now that the market has tumbled, these acquisitions just look awful. I want to see management commentary after this upcoming quarter, but if I don’t feel confident, I will be selling off the rest of my shares.

POOL- I bought a single share of Pool Corp in mid December. Pool is the leading distributor of swimming pool supplies and parts. They sell to contractors, pool retailers and pool owners amongst a myriad of others. Distribution is a fantastic business and Pool is second to none. They have fantastic returns on capital and have a lengthy record of consistent success. Simple but immensely profitable business model.

AMZN- I presume Amazon needs no introduction, but until recently,I had never held any shares. The stock saw a sharp drawdown in 2022, down almost 50% from the start of the year, presenting myself and others with a potentially great opportunity. I think the market is being shortsighted and Amazon is a business unlike any other. They are simply the most dominant business in the world and the one I would least like to compete against. They invest heavily into their business, spending $66B in R&D and $66B in CapEx in 2022. That is a wild amount of money spent in order to widen their moat. Just imagine how dominant they will be 10 years from now. I think they know exactly what they are doing, time will tell.

AMAT- I decided to pick up another share of Applied Materials in mid December after the stock had fallen 10% in a single day on the back of no real news. I’ve held shares in the company for a bit of time now, so picking up an additional share was a no brainer. Great business with fantastic execution and discipline.

As always, I would like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Best way to reach me is on Twitter, follow me @TheGarpInvestor.