Summer is here and I hope you all are making the most of it. Much of the United States is vaccinated and life finally feels like it is returning back to normal. We are not completely out of the pandemic woods yet, but we are certainly heading in the right direction. Markets continue to boom and the economy sure feels like it is heating up. The government stimulated the economy with trillions of dollars and all that money flowing around needs somewhere to go. Inflationary pressures are pushing prices up, seen particularly in areas such as lumber and other building materials.

While some of these price changes will be temporary, they are important to take note. How will they impact our companies and what price fluctuations are set to last into the future? I don’t necessarily have the answers to these questions, but it is our job as investors to sit around and ponder. I can postulate over various outcomes, but as usual I come to a similar conclusion; invest in great companies that can weather any economic environment. These companies are able to pass rising costs onto their customers while maintaining strong margins.

I have partnered with the great group at 7 Investing and become an affiliate. They offer monthly stock recommendations and so far they have absolutely crushed the market. For only $17 a month, you get access to their 7 best picks each and every month, one from each of their 7 lead advisors. Follow this link and use coupon code GARP to save $10 off your first month. I highly recommend their service!

Q2 Performance

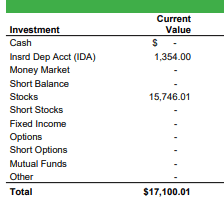

As of 7/1/2021, my 10K portfolio climbed to $17,100.01. When I started on 8/19/18, the SPY had a price of $285.06 and my account started with $10,000. As of 7/1/2021 the SPY had a price of $430.43. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation.

| | 10K Return(1) | SPY Return(2) | Difference(1-2) |

| 2018(8/19-12/31) | (13.95) | (13.71) | (.24) |

| 2019 | 37.33 | 32.6 | 4.73 |

| 2020 | 21.22 | 17.59 | 3.63 |

| 2021(1/1-6/30) | 19.38 | 17.5 | 1.76 |

| Since Inception(8/19/18) | 71 | 59.05 | 11.95 |

2021 continues to deliver more than satisfactory returns, both for myself and the S&P 500. After a strong 2019 and 2020, I did not expect another 20% gain in the first half of the 2021, but I’m not going to complain. I have maintained my outperformance over the S&P, with the delta now growing to just under 12% since inception. This isn’t exceptional, but I’ll take it. I will never add a dime to this portfolio, but I am constantly adding new money to my personal portfolios and I hope you do the same. If you can just outperform the markets by a small amount, over the course of decades it can compound into vast fortunes. Time in the market is the most important variable.

As I have noted before, while good, my performance is not all that great thus far. While I have beaten the S&P, I have lost handily to the Nasdaq. I would have been better off just buying the QQQ’s and learning to play golf. Since I started, investing in the QQQ’s would have provided returns of 101.72% beating me by 30.72%. I’m hoping that over time I can close the gap, but the Nasdaq is a tough competitor. Time will tell.

As we can see, my cash allocation has risen to $1,354. This comes out to around an 8% cash position. This is higher than I generally like to carry, so do not be surprised if I make a transaction somewhat soon. I have my eye on a few companies and a buy could be coming up.

Transactions

MCO- At the end of April, I bought 2 shares of Moody’s. Moody’s is a company I had long followed, but had never owned any shares of. As a company Berkshire Hathaway invested heavily into, Moody’s is well known to the investment world. Berkshire owns roughly 13% of the company and Warren Buffett has often talked about how much he admires the company and why their economics are so strong.

Primarily, Moody’s is a rating agency. They rank the creditworthiness of companies that intend to issue bonds to the public market. Before a company can go to the market with a bond issuance, they must get a credit rating from one of the licensed major credit rating firms. Moody’s along with S&P Global and Fitch Ratings, form an oligopoly in the industry. The three of them providing over 90% of all credit ratings. Many have tried to enter the space and unseat the legacy businesses, but all have failed. The three companies are utterly entrenched within the financial world.

Moody’s has a long and storied history, as they were founded by John Moody over a century ago. The company has gone through many iterations with different ownership structures over the years, coming to be owned by Dun and Bradstreet for decades. In 2000 they were spun off back into their own independent company, if only I had been smart enough as a 9 year old to buy in. Since 2000, the company would have returned over 53 times the initial investment with dividends reinvested.

Financially, the company is a rockstar. They support gross margins over 70% and those margins follow down to the bottom line at over 35%. As is a trend with companies I like to invest in, the business takes almost no additional capital to run. In 2020, they cash flowed around 2 billion, while only needing to spend 103 million on capital expenditures. This leaves a lot of money with which to reward shareholders. In 2020 they paid out 420 million in dividends, bought back 556 million worth of shares, and made acquisitions that added up to just under 900 million. They followed suit this past quarter doing more of the same while adding cash to their strong balance sheet.

Speaking of this past quarter, they divulged a particularly strong report and I saw an opportunity to buy into such a well built growing business. In Q1, Moody’s saw revenue growth of 24% and adjusted EPS growth of 49%. Not too shabby for a company that’s been around since before WW1. So far I have been rewarded, my shares are up 13.65% after only a couple of months. Let’s hope they keep up the momentum!

EGHSF- At the end of June, I sold my shares of Enghouse Systems. I have long admired the company, but their most recent quarterly report made me question some of their decisions. Once you lose a little conviction, it is hard to remain invested in the company. I don’t do half measures, I’m either in or out.

Revenue this past quarter fell 16% as compared to the previous year. I call myself the GARP investor for a reason. I am looking for companies with growth, not slipping in the opposite direction. To be fair, Enghouse was running up against comps that were inflated due to how well their Vidyo business performed at the start of the pandemic. That business has since tailed off, returning back to PreCovid numbers. Part of my issue with the company is how reliant they are on Vidyo. In the world of Zoom, I’m just not convinced Vidyo provides a strong enough differentiating platform. They have invested a lot of money into Vidyo’s success and it might turn out to have all been a waste.

Enghouse has also publicly bemoaned their inability to get as many acquisitions done as they would have liked. They cite higher prices and a general slowdown in transaction speed due to the pandemic. I think these are valid claims, but when I compare them to another portfolio company of mine, Constellation Software, Enghouse comes out inferior. Constellation has had no trouble closing deals, I seemingly read about multiple acquisitions they close every single week.

Admittedly, I might look back at this as a foolish decision full of recency bias. They have been a strong performer in the past and their CEO Stephen Sadler is well respected for a reason. Given all the variables placed in front of me however, I think I have better opportunities to invest those dollars. I’ll be sure to revisit this decision in the future.

As always, I would like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Follow me on Twitter @TheGarpInvestor.