First off, I’d like to apologize that this update is coming out quite a bit later than I would normally prefer. I was away on a vacation, then had to catch up on work at my business. It has been a particularly stressful period at work and I simply didn’t have the time or mental energy to type up this update.

It is also difficult to write a financial update after a quarter such as this past one. Losing money in investments is heart wrenching. There is no getting around that. It is especially difficult for me, because I have chosen to post my investments publicly and open myself up to ridicule.

I find myself questioning if I really know what I am doing. Am I an imposter posing as a credible investor? Did I do enough investment research or act impulsively? Are the companies I’ve chosen strong enough to withstand an economic recession? Are my investments too correlated and therefore subject to the same risks?

Well, only time will tell us the answers to these questions. In the face of adversity, there is of course only one proper course of action and that is to carry on. Wallowing in sorrow does nothing to improve the situation. Make use of market volatility and kick your research process into high gear and start turning over every stone. Fortunes are won and lost during tumultuous times. Do your best to find yourself sitting on the winning side of the equation. Blood in the streets breeds opportunity. There are high quality companies out there trading at multiples not seen in a decade.

Q2 Performance

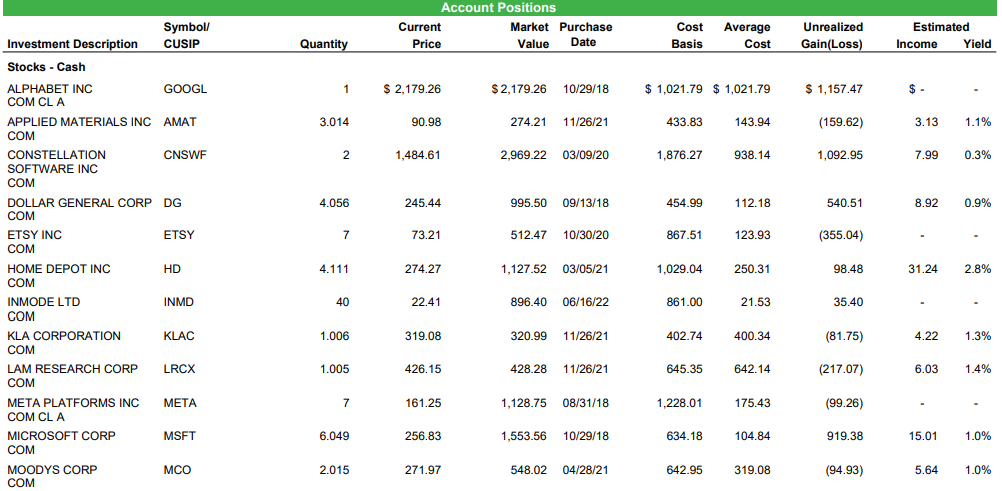

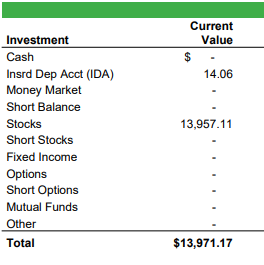

As of 7/1/2022, my 10K portfolio is worth $13,971.17. When I started on 8/19/18, the SPY had a price of $285.06 and my account started with $10,000. As of 7/1/2022 the SPY had a price of $381.24. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation

| 10K Return(1) | SPY Return(2) | Difference(1-2) | |

|---|---|---|---|

| 2018(8/19-12/31) | (13.95) | (13.71) | (.24) |

| 2019 | 37.33 | 32.6 | 4.73 |

| 2020 | 21.22 | 17.59 | 3.63 |

| 2021 | 38.55 | 28.43 | 11.52 |

| 2022(1/1-6/30) | (29.60) | (19.61) | (9.99) |

| Since Inception(8/19/18) | 39.71 | 42.88 | (3.17) |

| CAGR | 9.12 | 9.68 | (.56) |

2022 has proven to be an incredibly difficult investing period. My portfolio has gotten crushed, down just a hair under 30% this year. Even worse, I have lost to the market by a rather significant margin. Going into the year I was outpacing the market by a healthy amount, but after a 9.99% loss in 2022, I find myself trailing the S&P since inception. I don’t care so much that my portfolio has gone down, but I do care about losing to the market. Why spend the time and effort if I am unable to beat the index? Let’s hope in the long term this trend reverses and I can get back out on top.

The economy appears to be on the brink of a recession, with few positives to rely on.. I don’t like to make market predictions, but all indicators are pointing downwards. Is this already priced in? I have no idea. The market could rebound and turn positive in the back half of 2022 or just as easily fall another 20-30%. Rather than try and time market movements, I believe the right course of action is to focus on picking quality companies with high returns on invested capital trading at reasonable prices.

Transactions

NTDOY- In mid June, I decided to make a couple of changes within my portfolio after seeing some particularly attractive opportunities. My portfolio was already fully invested, so I needed a way to raise money. After examining my companies, I determined that Nintendo was the one that had to go.

I sat on a slight loss, so there were no tax burdens to take into account. Actually I will be able to use that loss to offset the gains from selling shares of Dollar General which I will talk about below. I still really like Nintendo and think they have a great future in front of them. They are incredibly profitable with strong margins and boast what is probably the best IP in the entire video game universe. I have just begun to worry about the growth prospects and what the next phase will bring. Growth has gone in the wrong direction and the company has not laid out a roadmap of what exactly to expect in the future. A lot of variables are on the table that have to be taken into account. Don’t misunderstand however, I am still a believer in the company. I continue to own shares in accounts outside of this blog,

DG- I also decided to trim my position in Dollar General. No real problem here, I just needed to raise more cash. Dollar General stock had gone up quite a bit and was trading at a hefty premium to the overall market. I still love the company and want to remain a shareholder, but rebalancing and taking some off the table isn’t the worst outcome.

ULTA- I have long admired Ulta, but never saw a good opportunity to pick up some shares. Ulta is a very high quality retail chain selling affordable beauty products. This market downturn finally opened up an opportunity to buy Ulta at a reasonable price. As long as I’ve followed them, the company traded for over 30 times free cash flow. Ulta came roaring out of the pandemic, as women could finally go back out in public and beauty products flew off the shelves. I bought Ulta for roughly 18 times free cash flow. They are a remarkably consistent company, growing revenue, net income and free cash flow virtually every year. They operate a simple business model, open high return stores each year and use the free cash flow to repurchase shares. Share count has fallen from 64.65 million in 2015 to 53.94 million today, a 16.57% reduction.

There is also a longstanding psychological trend called the lipstick effect. In times of recession, women are found to spend money on small indulgences like lipstick and other beauty products, as they forego large expenses like foreign travel or a kitchen redesign. A splurge on a premium beauty product is unlikely to break the wallet, while providing a quick dopamine hit. Given the murky future our economy seems to be heading towards, I feel comfortable holding such a high quality steady company.

INMD- In mid June I decided I couldn’t wait any longer and pounced on some shares of InMode. On financials alone, I personally cannot find a single company that provides a better opportunity. They check every single box I look for and do so with flying colors. High and growing margins? You bet. Low capital intensity? Only $1 million of CapEx on $170 million in operating cash flow. Strong balance sheet? $400 million in cash against only $61 million in total liabilities, not just debt. Ex-cash, the company trades for about 10 times trailing twelve months free cash flow.

Where’s the rub? Well, InMode sells minimally invasive medical products. If you are an astute reader of mine, you will know that I am not a medical doctor. In fact, I have absolutely no medical training at all whatsoever. I can’t really tell you what their products do, or how they compare to their competitors in the market. Could their products become outdated and replaced in the future? Sure. Could a competitor create a superior product and replace them as a market leader? Definitely. All I know is that the market can’t seem to get enough and sales are exploding. If I had to pick one company that I think has a good chance of becoming a 10 bagger, InMode is the one. Perhaps I am foolish for betting on a company with these kinds of unknowns, but I’m willing to risk it.

As always, I would like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Best way to reach me is on Twitter, follow me @TheGarpInvestor.