If Q1 was defined by shock, Q2 was defined by the market’s almost unsettling ability to move on.

The war in the Middle East did not disappear. Oil remained volatile. Inflation fears returned. The Federal Reserve stayed cautious. And yet, despite all of that, the S&P 500 finished the quarter near all-time highs, closing June around 7,500 after rebounding from the March lows.

That is the strange thing about markets. They do not wait for the world to feel safe. They do not wait for the headlines to become tidy. They bottom when the future is still unclear, and they often rise while the average person is still trying to understand what just happened.

Oil, War, and the Market’s Memory

Coming into Q2, the fear was simple: the conflict with Iran would keep oil prices elevated, reignite inflation, squeeze consumers, and force the Fed into a more hawkish stance. That was not an unreasonable concern. When a large portion of global energy supply is threatened, the consequences can be dire.

But as the quarter progressed, the worst-case scenario began to fade. There were still flare-ups, still threats, still the kind of headlines that make investors nervous. But oil prices came down from their panic highs, and the market increasingly treated the war as a serious but containable event.

Whether that is wise remains to be seen.

One of the uncomfortable truths about investing is that markets often look cold-blooded. Human beings see war, suffering, risk, and uncertainty. Markets see probabilities, liquidity, earnings, and whether the next data point is better or worse than feared.

And in Q2, “better than feared” was enough.

Earnings

The simplest explanation for the market’s strength may also be the least dramatic: earnings held up. For all the focus on war, oil, and rates, corporate America continued to do what investors ultimately need it to do. Let earnings grow and compound. That does not mean the market is cheap. It does not mean risks have disappeared. But it does help explain why stocks were able to look past so much bad news. Investors can tolerate a messy world when profits are still moving in the right direction.

This is an important point because it cuts against the more satisfying narratives. It is tempting to say the market rallied because the war cooled down, or because investors expect easier monetary policy, or because AI remains unstoppable. All of that may be true in part. But markets are usually less poetic than that. If earnings estimates are rising, margins are holding up, and companies are guiding with confidence, stocks have a reason to climb. The world can feel unstable while the income statement looks surprisingly healthy. That tension defined much of Q2.

Of course, this cuts both ways. Higher earnings expectations are not just a support for the market; they are also a hurdle. Once investors price in resilience, resilience is no longer enough. Companies have to beat, guide higher, and convince investors the next few quarters still justify the move. That is the risk in a market sitting near all-time highs. The rally may have been rational, but it has also raised the bar for further execution.

Q2 Performance

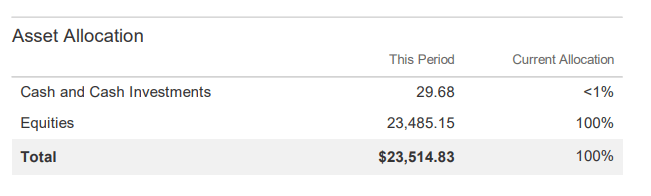

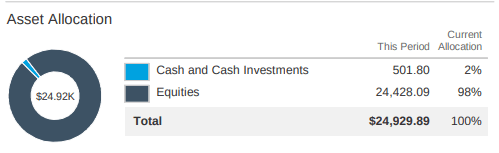

As of 7/1/2026, my 10K portfolio was worth $36,121.13. When I started on 8/19/2018, the SPY had a price of $285.06 and my account started with $10,000. As of 7/1/2026 the SPY had a price of $745.76. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation.

| Year | 10K Portfolio | SPY | Outperformance |

|---|---|---|---|

| 2018 (8/19–12/31) | -13.95% | -13.71% | -0.24% |

| 2019 | 37.33% | 32.60% | 4.73% |

| 2020 | 21.22% | 17.59% | 3.63% |

| 2021 | 38.55% | 28.43% | 10.12% |

| 2022 | -27.25% | -18.65% | -8.60% |

| 2023 | 41.36% | 26.72% | 14.64% |

| 2024 | 21.39% | 25.59% | -4.20% |

| 2025 | 19.26% | 18.00% | 1.26% |

| 2026 (1/1–3/31) | -6.03% | -4.54% | -1.49% |

| 2026 (4/1–6/30) | 30.16% | 14.26% | 15.90% |

| Since Inception (8/19/18) | 261.21% | 195.46% | 65.75% |

| CAGR | 17.73% | 14.77% | 2.96% |

I’d have to dive in and look more closely to confirm, but Q2 of 2026 was likely the best single quarter my portfolio has ever seen. My portfolio was up a mind-boggling 30.16%, against a still very respectable 14.26% for the SPY. This is partially due to timing. My portfolio happened to hit a low for the year exactly when Q1 ended, and climbed rapidly all throughout Q2.

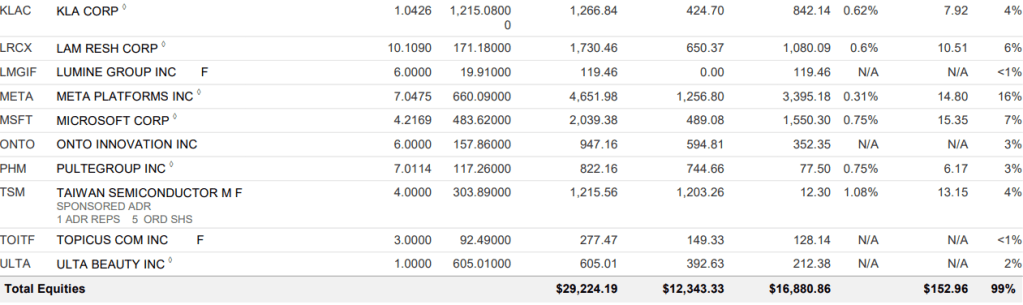

Semicaps

I have not been shy about my love for a particular sector: semicaps.

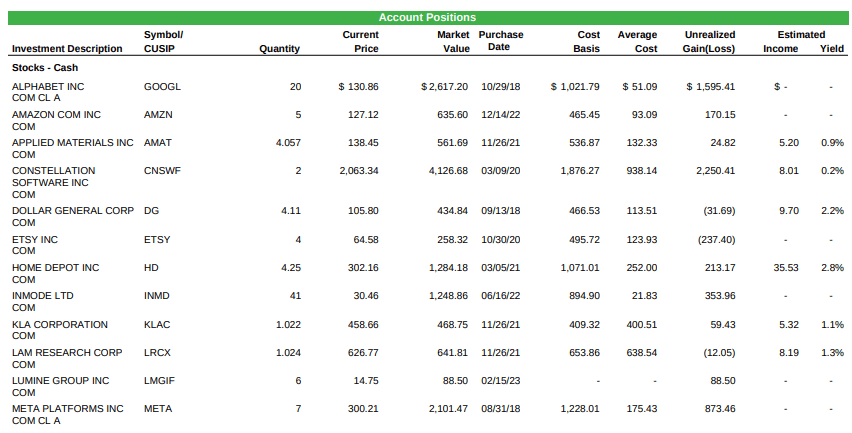

As I’ve written before, semicaps are semiconductor capital equipment companies. They are, as a group, a wonderful collection of businesses. High returns on capital, strong competitive positions, growing revenue, and free cash flow profiles that most companies could only dream of. NVIDIA, Taiwan Semi, Apple, AMD, Broadcom, and the hyperscalers could not exist in their current form without them. They are the boring picks and shovels behind the AI boom.

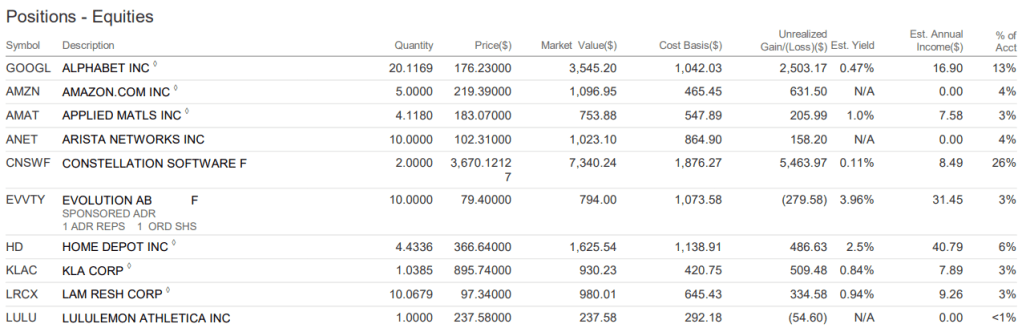

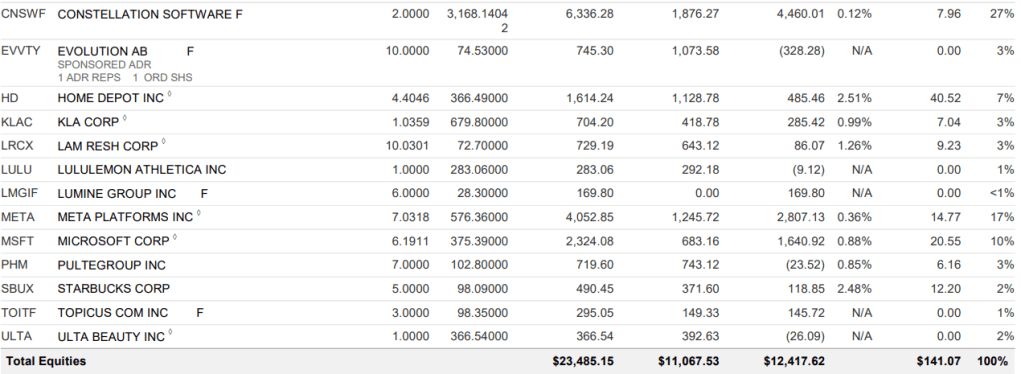

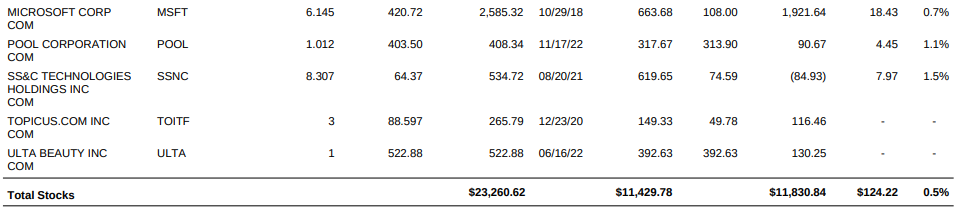

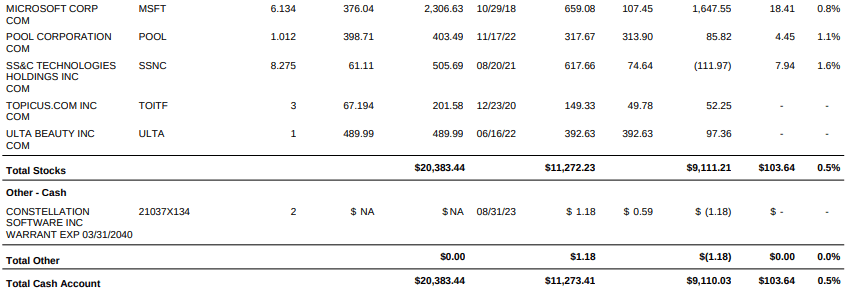

In my portfolio, I’ve owned four semicaps: Applied Materials, KLA, Lam Research, and Onto Innovation. To say their stock performance this past quarter was extraordinary would be a massive understatement.

That is not normal.

And frankly, it makes me nervous.

My view on the quality of these businesses has not changed. If anything, the long-term importance of the sector has become more obvious. But there is a major difference between recognizing a great business and paying any price for it. Stock prices have moved far faster than earnings, and in many cases the multiples now look stretched, if not outright ludicrous.

When companies trade in line with earnings growth, that is healthy. This feels different. This feels like exuberance. Investors have begun treating cyclical industrial businesses as if they are poised for unstoppable growth, and that changes the risk profile. At that point, future returns depend less on being right about the business and more on the crowd staying excited.

I still love the companies. I am simply less enthusiastic about the stocks. Some trimming may be warranted, not because the thesis is broken, but because the market has moved from underappreciation to something much closer to euphoria.

Transactions

I had an uncharacteristically busy quarter, with multiple purchases and sales. I generally espouse long term ownership of stocks and infrequent trading, but sometimes the market provides opportunities and an investor needs to make the best decision given in front of them. Given the number of transactions I made, I’ll keep commentary brief.

Exits and trims

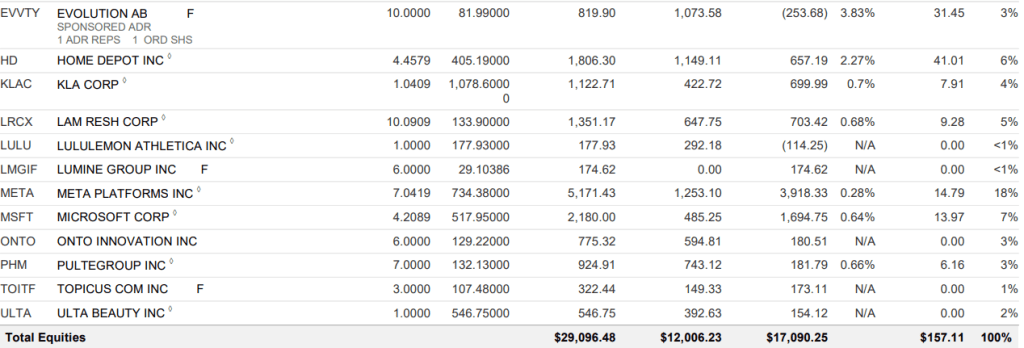

- EVO- Sold: The company remains attractive, but regulatory and business-model risks created too many variables for my comfort.

- PHM and HD- Sold: Higher rates and weak housing turnover have created persistent headwinds. Both remain good businesses, but I saw better opportunities elsewhere.

- ONTO- Sold: The valuation approached nearly 100× free cash flow, which became impossible for me to justify.

- LRCX and KLAC- Trimmed: Reduced oversized semicap exposure and funded new purchases.

New positions

- RDDT: Rapid growth, gross margins above 90%, and substantial long-term cash-flow potential.

- MA and SPGI: Two exceptional, capital-light businesses purchased at valuations that finally looked attractive after years of high multiples.

- BKNG: The leading travel booking platform with exceptional margins, strong cash generation, and rapidly rising operating income.

- VEEV and INTU: High-quality software businesses caught in broader SaaS weakness, creating more attractive entry points. I believe their entrenched market positions and mission-critical products will prove more resilient to AI disruption than current valuations imply.

None of this changes how I think about investing: find great businesses, understand what you own, and let time and compounding do the heavy lifting. But with the market pricing in a lot of good news and parts of my own portfolio reflecting real exuberance rather than just quality, I’m entering Q3 a bit more selective about where I add and more willing to trim into strength than I’ve been in years. The businesses remain excellent, my job now is just not to overpay for that excellence.

As always, I would like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Best way to reach me is on Twitter/X, follow me @TheGarpInvestor.