The clock has officially run out on 2025. It’s a strange feeling stepping out of a year that many expected to be a train wreck, only to watch the markets finish on a note of almost casual defiance. If 2024 was defined by the agonizing wait for the shoe to drop, 2025 was the year we realized the shoe might never fall, while still remembering that gravity hasn’t gone away.

Year-end reflection is a ritual, but as we enter 2026, the fog feels thicker than usual. The pillars we once leaned on for certainty, legendary leaders, “sticky” business models, and the predictability of code, have all been called into question. I don’t have a crystal ball for 2026, but I do have a healthy sense of curiosity and a portfolio built to withstand surprises, not predict them.

The Discipline of Less

What Q4 reinforced wasn’t a new way of thinking, but the growing importance of restraint.

Markets reward activity. They provide a constant stream of “breaking” news to encourage opinions on everything, creating the illusion that staying informed is the same thing as making progress. Over time, I’ve found the opposite to be true: The most valuable skill an investor can possess isn’t knowing more; it is knowing what to ignore.

Earlier in my journey, I felt a restless need to master every industry: pharma, regional banks, biotech, quantum computing. I thought complexity was where the edge lived. In reality, it just scattered my attention and built a foundation of false confidence.

Today, I deliberately shrink my investable universe. Entire sectors are excluded without debate. I move on immediately from companies in high-regulation or high-complexity fields. Not because they can’t generate returns, but because they demand an expertise I don’t have and won’t pretend to. Complexity deserves respect. Some businesses are won through scientific breakthroughs or regulatory nuance; I prefer arenas where outcomes hinge on durable economics, aligned incentives, and business models that a ten-year-old could explain.

Systems That Endure

In December, I visited the Panama Canal. Watching 100,000-ton vessels move inch-by-inch through a lock system first conceived over a century ago was a visceral reminder of the power of a “toll-bridge” asset.

What stood out wasn’t that the canal never changes, but that it adapts specifically to protect its monopoly. The recent expansion, which added new locks and lanes to handle larger ships, wasn’t reinvention for its own sake. It was a pragmatic investment to protect relevance.

At its core, it’s geography turned into an economic engine. Ships pass through because there’s no comparable alternative, allowing Panama to collect small fees on enormous volumes of global trade. Seeing it in person reinforced a core principle: the best businesses don’t try to outrun the future. They invest so the future is forced to pass through them.

Fewer Bets, Higher Conviction

Shrinking the universe naturally changes how capital is deployed. Fewer ideas demand higher standards. Higher standards lead to concentration, and concentration forces accountability. Every position has to earn its place.

This isn’t about taking more risk, it’s about avoiding unforced errors. Risk isn’t volatility; it is the permanent loss of capital caused by being wrong about a business’s nature. Knowing what you don’t know is one of the few edges that actually compounds over a lifetime.

2025 ended with a roar. Maybe that momentum carries into 2026. Maybe the “shoe” finally hits the floor. Either way, my focus remains on clarity over cleverness, process over prediction, and patience over activity. I don’t need more ideas. I just need the right ones and the discipline to wait for them.

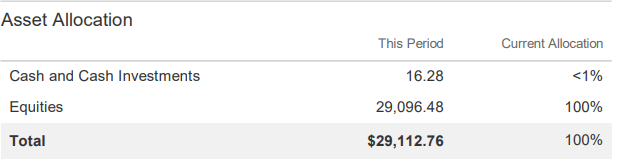

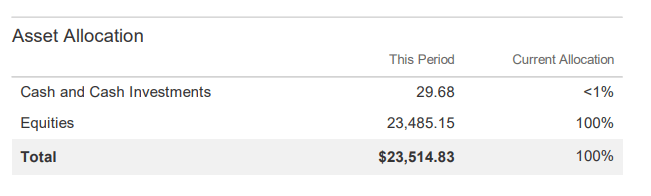

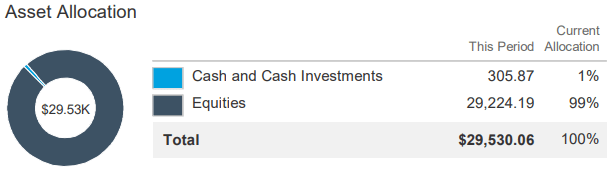

As of 1/1/2026, my 10K portfolio was worth $29,530.06. When I started on 8/19/2018, the SPY had a price of $285.06 and my account started with $10,000. As of 1/1/2026 the SPY had a price of $681.92. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation.

| Year | 10K Portfolio | SPY | Outperformance |

|---|---|---|---|

| 2018 (8/19–12/31) | -13.95% | -13.71% | -0.24% |

| 2019 | 37.33% | 32.60% | 4.73% |

| 2020 | 21.22% | 17.59% | 3.63% |

| 2021 | 38.55% | 28.43% | 10.12% |

| 2022 | -27.25% | -18.65% | -8.60% |

| 2023 | 41.36% | 26.72% | 14.64% |

| 2024 | 21.39% | 25.59% | -4.20% |

| 2025 (1/1–3/31) | -5.03% | -3.76% | -1.27% |

| 2025 (4/1–6/30) | 19.11% | 10.43% | 8.68% |

| 2025 (7/1–9/30) | 3.93% | 8.52% | -4.59% |

| 2025 (10/1–12/31) | 1.00% | 2.31% | -1.31% |

| Since Inception (8/19/18) | 194.06% | 168.37% | 25.69% |

| CAGR | 15.76% | 14.33% | 1.44% |

Q4 was not a great quarter for my portfolio, lagging the SPY by 1.31%, but that is hardly a tragedy. Zooming out, 2025 was a fantastic year for my portfolio. I finished up 18.75%. I would happily lock that in for the rest of my life.

In gross dollars, I was up $4,644.50, about a 46% gain on that initial $10,000 I started with. Compounding is magic. It just needs time and a little emotional discipline not to screw it up.

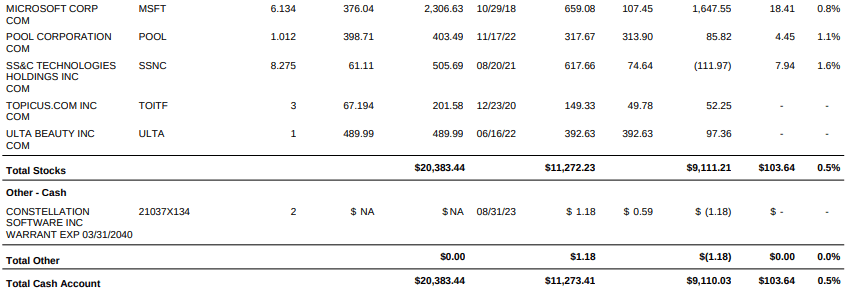

The Constellation Dilemma: A Proxy for the Future

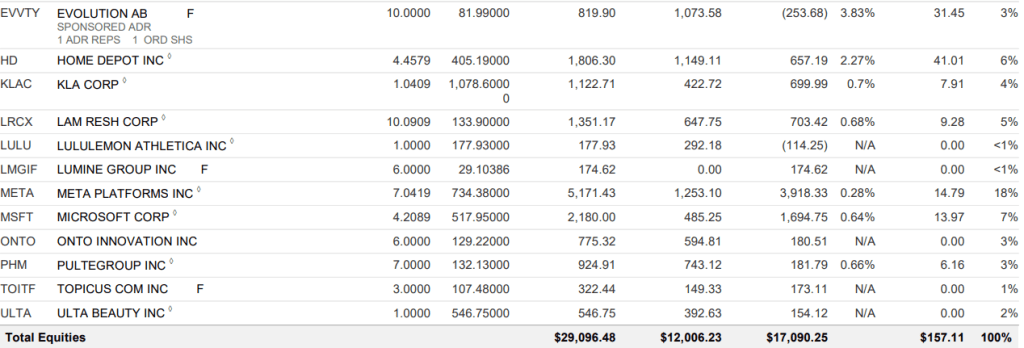

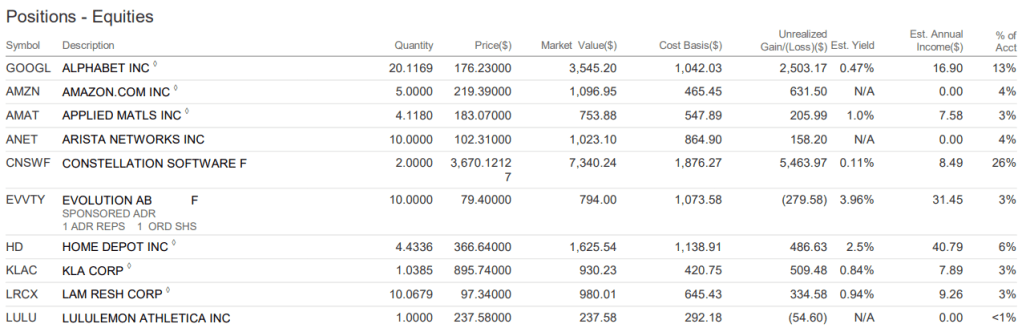

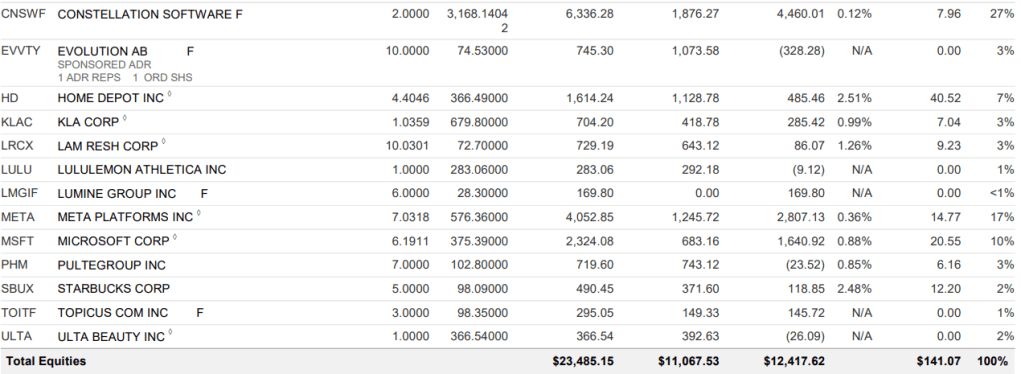

The defining debate in my portfolio right now centers on Constellation Software.

For thirty years, it followed a a near-perfect playbook: buy niche, mission-critical software companies, leave them alone, and reinvest the cash. But in late 2025, that trajectory snapped. The stock shed nearly 45% of its value as a “double whammy” hit the ticker: the abrupt retirement of founder Mark Leonard for health reasons, combined with a growing panic that generative AI would turn its portfolio of niche software into a collection of overpriced relics.

The bear case is straightforward. If an AI agent can write a custom billing system for a small-town utility for pennies, Constellation’s high-margin moats evaporate. The market is now pricing $CSU as if it’s on the wrong side of an AI propelled asteroid.

This fear was amplified by Leonard’s exit. For many, Leonard was the thesis. A brilliant conductor standing before an orchestra he built from scratch. Without his disciplined hand on the tiller, investors are questioning whether the decentralized machine he built can still identify value in a world where the very definition of “software” itself is being rewritten.

The Rational Reset

It’s tempting to label a 45% drawdown as pure market panic. In this case, the correction feels largely rational.

For years, Constellation traded at a perfection premium, a valuation that assumed Mark Leonard would remain at the helm indefinitely and that the moat of VMS was impenetrable. Late 2025 challenged both assumptions at once. This wasn’t a glitch. It was a re-rating of what certainty is worth in a world that just got more uncertain.

That doesn’t mean the company is dead.

At today’s price, Constellation has shifted from an expensive legend to a balanced bet on execution. The machine Leonard built is now in the hands of Mark Miller, a 30-year veteran who founded the company’s very first acquisition. Free cash flow is still pouring in. Capital is still being reinvested. But the narrative has moved from inevitability to possibility.

As we enter 2026, the path forward is essentially binary.

If Miller maintains the culture of hurdle-rate discipline while navigating the AI transition, this will be remembered as a generational buying opportunity. If the bears are right and AI agents begin rapidly displacing legacy VMS systems, this 45% drop may just be the opening chapter of something much uglier.

For now, the price feels rational. I’m content to watch execution, hold my shares, and not pretend I can predict which branch of that forked road we’re actually on.

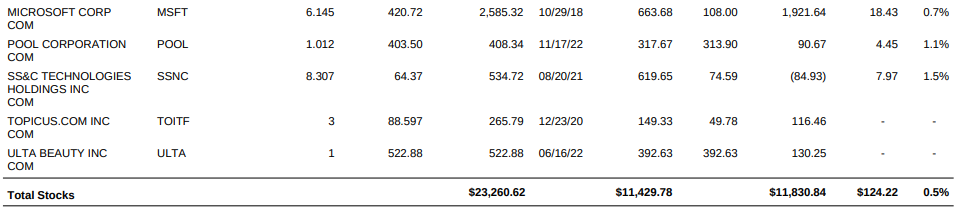

Transactions

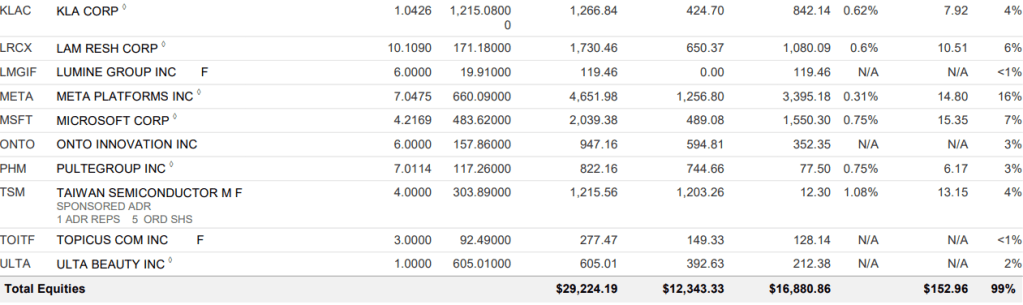

TSMC- I started a position in Taiwan Semiconductor this quarter.

It’s hard to overstate how central this company is to the modern world. TSMC isn’t just another chip business, it’s arguably the most important company on the planet. Every major AI breakthrough, smartphone upgrade, data center expansion, and next-gen chip design eventually bottlenecks through their fabs. If silicon is the new oil, TSMC is the Saudi Aramco of the digital age.

What makes the story so compelling is that TSMC sits at the intersection of insatiable demand and near-impossible supply. Apple, Nvidia, AMD, Qualcomm, and the hyperscalers are all fighting for limited cutting-edge capacity. Even in slowdowns, TSMC’s most advanced nodes stay fully booked.

That’s because TSMC is an irreplaceable choke point in the semiconductor ecosystem. Designing chips is hard. Manufacturing them at scale, at leading-edge yields, is borderline insane. The capital costs are staggering, the learning curves are brutal, and the process knowledge compounds over decades.

The economics reflect that reality. Operating margins around 50% are absurd for a manufacturing business. Even while spending tens of billions a year on capex, TSMC still throws off massive free cash flow. The balance sheet is one of the strongest on earth, they sit on roughly $97B in cash and equivalents.

This isn’t risk-free. Geopolitics is a permanent storm cloud, and I’ll let others opine on the China-Taiwan situation. Capex intensity is extreme. Should demand ever meaningfully falters, earnings would get hit fast. That said, TSMC is so far ahead of any competitor that it could probably stop investing for years and still own the world’s best fabs.

Given the economics and the sheer dominance of the business, I’m willing to live with the risks.

HD and GOOGL- I trimmed my holdings in Home Depot and Google. Not to much to write about this, I needed to free up some capital to buy Taiwan Semi and something had to go.

LULU- I decided to exit my position in Lululemon.

It’s still a phenomenal brand, just one that’s hit a rough patch. A mid-December pop in the stock, driven by a holiday guidance bump, gave me a clean window to step away.

On paper, the metrics still look fine: under 20x free cash flow, a strong balance sheet, and aggressive buybacks. If this were a spreadsheet-only decision, I’d probably still own it. The problem is the narrative.

Lululemon is at a real crossroads. The entire athletic apparel space is in a lull, just look at Nike and Under Armour. Lulu is also facing new competitive pressure. Fashion-forward upstarts like Alo and Vuori are chipping away at its premium positioning, while dupe culture is quietly commoditizing its core products. When a solid alternative is sitting at Costco for a quarter of the price, the Lulu premium gets harder to defend.

Could they turn it around? Absolutely. But it’s not a battle I need to be in. Fashion is brutally competitive, brand moats are fragile, and there are easier places to compound capital without having to guess what people will want to wear three years from now.

As always, I would like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Best way to reach me is on Twitter/X, follow me @TheGarpInvestor.