The second quarter of 2025 began with a thud.

Markets fell hard in early April, spooked by persistent inflation and the lingering threat of new tariffs. Investor sentiment, already fragile from Q1’s grind, cracked under the weight of more uncertainty. For a moment, it looked like the bottom might give out entirely.

Then, almost inexplicably, the market reversed.

There was no major economic shift. No rate cut. No breakthrough on inflation. But over the course of the quarter, the S&P clawed its way not just back to prior levels, but to fresh all-time highs. It was a rapid climb built on improving sentiment. The panic around tariffs began to ease. Political rhetoric softened and investor confidence soared.

Markets don’t always need great news to rise. Sometimes, they just need the bad news to stop getting worse.

The Breakup No One Could Have Possibly Seen Coming

Elon and President Trump broke up. They shocked the world, ending the greatest romance of our time. Apparently, when you combine the two biggest egos on the planet, even love isn’t enough.

Of course, we all knew this was coming, it was never a matter of if, but when. And interestingly, it wasn’t President Trump who threw the first punch. It was Elon.

Frustrated by the Big Beautiful Bill’s attack on EV tax credits, and perhaps realizing that DOGE was not as effective as he would have hoped, Elon lashed out publicly. In a now infamous Tweet, Elon claimed Trump to be on the Epstein list. Trump responded in kind, and soon the whole thing devolved into a gloriously public feud.

It’s entertaining, sure, but also meaningful. And while Elon often acts like he’s above politics, he’s very much inside the game. Meanwhile, the President doesn’t take betrayal lightly, so beware what this might mean for any company Elon is involved with.

So yes, it is a breakup. Yes, it was inevitable. But when the President and the richest man on Earth start taking shots at each other, investors should pay attention. The stakes aren’t just personal, they’re political, financial, and potentially market-moving.

The Magnificent Seven Out of Sync

Once hailed as the dominant engine of the market, the “Magnificent Seven” are no longer moving in lockstep. This quarter brought separation.

- Apple struggled with slowing sales in China and regulatory scrutiny.

- Google got dinged by AI concerns and existential questions around the future of search.

- Tesla continued to bleed, caught between rising EV competition, margin compression, and Elon’s increasingly scattered focus.

That’s the bad news. What about neutral?

- Amazon as of June 30th, somehow finished the quarter exactly flat (0.0%). Statistically, I’m not sure how that is even possible. I can’t think of a more neutral sign, so the market is telling us Amazon is a hold.

The winners?

- Microsoft, Meta, and Nvidia haven’t flinched. Whether it’s cloud, chips, ads, or AI, they continue to dominate, print profits, and drive the index upward with terrifying efficiency.

And while we’re reassessing who really belongs in this elite club, one outsider might be making a push to get included. Netflix. Erasing any doubt, they’ve posted record profits, strong subscriber growth, and flexed pricing power. If there’s room for an “Elite Eight,” they’ve earned a seat at the table.

That being said, I would not bet against any of the Seven, with the possible exception of Tesla, which is clearly the most volatile of the bunch. These are still the biggest, most profitable companies the world has ever seen. Each investing billions to crush competition and deepen their grip on the financial system. They remain the axis around which the market spins.

Final Thoughts

This quarter was a lesson in patience, again.

The best investment decisions rarely feel good when you make them. Buying in March felt like catching a falling knife. Staying invested through April meant ignoring every bearish headline. But Q2 rewarded those who did nothing. Who endured and who held on.

It’s tempting to trade the noise, to react, to do something. But most wealth isn’t built by guessing right. It’s built by enduring well.

There will be a time when markets fall again. There will be more recessions, maybe even another depression someday. But unless the entire economic system collapses, markets recover. They always have.

Stay invested. Stay patient. Let the noise fade. Time does the rest.

Q2 Performance

As of 7/1/2025, my 10K portfolio was worth $28,010.80. When I started on 8/19/2018, the SPY had a price of $285.06 and my account started with $10,000. As of 7/1/2025 the SPY had a price of $617.65. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation.

| Year | 10K Portfolio | SPY | Outperformance |

|---|---|---|---|

| 2018 (8/19–12/31) | -13.95% | -13.71% | -0.24% |

| 2019 | 37.33% | 32.60% | 4.73% |

| 2020 | 21.22% | 17.59% | 3.63% |

| 2021 | 38.55% | 28.43% | 10.12% |

| 2022 | -27.25% | -18.65% | -8.60% |

| 2023 | 41.36% | 26.72% | 14.64% |

| 2024 | 21.39% | 25.59% | -4.20% |

| 2025 (1/1–3/31) | -5.03% | -3.76% | -1.27% |

| 2025 (4/1–6/30) | 19.11% | 10.43% | 8.68% |

| Since Inception (8/19/18) | 180.10% | 141.68% | 38.42% |

| CAGR | 16.17% | 13.71% | 2.46% |

This was surely one of, if not the best quarters I’ve had on record, both in total return and relative to the index. I finished the quarter up 19.11% and beat the SPY by 8.68%. I don’t expect this type of performance to be the norm, it was clearly anomalous, but I’ll gladly take it.

The rally was broad across my holdings. Some of the gains were driven by multiple expansion, but much of it reflects the strength of the underlying businesses. These aren’t speculative names riding hype cycles, they’re durable cash-generating machines with real competitive advantages. I remain hopeful for continued outperformance, but more importantly, continued execution.

Transactions

MSFT– I trimmed a couple of shares of Microsoft. Nothing dramatic, the company continues to execute exceptionally well, particularly in cloud and AI. But with the stock running hot and the position growing oversized, I wanted to free up some capital for a new high conviction idea.

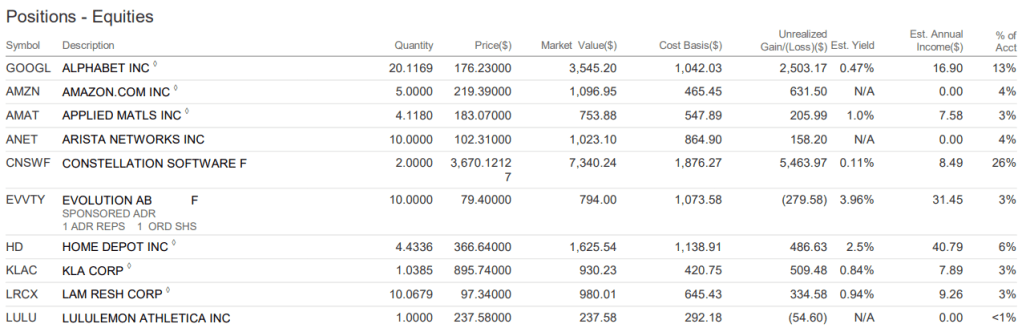

ANET- I used that capital to initiate a position in Arista Networks, a business that I believe exemplifies what a modern compounder looks like.

ANET is one of the most quietly dominant businesses in the market. They’ve taken meaningful market share from Cisco by focusing on high-performance networking equipment, primarily for data centers, and they’re riding major secular tailwinds: AI infrastructure, cloud migration, and enterprise network upgrades.

But what makes Arista truly exceptional is its economics. Gross margins near 65% and operating margins that have gone up every year, now at 42%. Arista has a fortress for a balance sheet, sitting on over $8B in cash, with only $4.4B in total liabilities. Every metric points in the same direction, up and to the right.

Growth has been consistent, capital allocation has been disciplined, and the business scales with impressive efficiency. When I finally found an opportunity to buy it at a reasonable multiple, I pounced. ANET has proven its compounding ability over the past decade, now I’m just hoping they keep the momentum going.

As always, I would like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Best way to reach me is on Twitter, follow me @TheGarpInvestor.