The sun has set on 2024 and just begun to rise on 2025, marking the threshold of a new chapter brimming with opportunities, challenges, and, as always, the ever-shifting tides of market sentiment. Reflecting on the year gone by and preparing for the road ahead is a timeless ritual. While we cannot predict the future, we can meet it with preparedness, curiosity, and resilience–traits that have served both investors and dreamers well throughout history.

Costa Rica

I spent a little over a week in Costa Rica around Christmas, and the country’s beauty is truly breathtaking. Towering rainforests alive with vibrant wildlife, pristine beaches meeting turquoise waters, and sunsets that feel like paintings—it’s a place where nature’s magic is on full display.

The Ticos, as Costa Ricans call themselves, embody the spirit of “Pura Vida.” More than a phrase, it’s a way of life—an embrace of gratitude, simplicity, and joy in the moment. Adventure is everywhere, and I made the most of it. I ziplined through lush canopies, hiked to cascading waterfalls, and even raced down what my resort claimed to be the world’s longest jungle waterslide.

But my most unforgettable moment came on a whitewater rafting trip down the Tenorio River. After a steep drop, our raft flipped, and I was thrown into the churning water, trapped beneath the raft as the waterfall above pummeled me. The force of the current was overwhelming, dragging me down no matter how hard I fought to resurface. My life jacket, meant to keep me afloat, seemed useless against the relentless pull of the river. Panic set in as my lungs burned and the seconds stretched into what felt like an eternity.

Just when I thought I couldn’t hold on any longer, a guide grabbed my life jacket and pulled me to safety. Gasping for air, heart pounding, I realized how close I had come to the edge. That moment has stayed with me—a stark reminder of nature’s raw power and life’s fragility. It taught me to cherish the small things—each breath, each heartbeat, each fleeting moment of calm—as gifts not to be taken for granted. Pura Vida isn’t just a saying; it’s a mindset. Costa Rica taught me to appreciate life’s fleeting beauty, a lesson I’ll carry long after leaving its shores.

Markets in 2024: A Tale of Two Realities

The markets demonstrated remarkable resilience in 2024, with indices reaching new highs. Yet, investor sentiment often felt curiously subdued—like a fire that burns brightly but doesn’t radiate warmth. Many approached the market cautiously, bracing for a correction that, for now, remains purely hypothetical. Indices have begun to surrender some of their recent gains, leaving investors wondering whether we are on the verge of a prolonged downturn or merely pausing before another rally.

The truth, as always, is that no one knows. Predictions are easy; preparation is harder. The wise investor focuses not on timing the market but on understanding the businesses they invest in, assessing valuations, and maintaining discipline. The market, after all, has never rewarded haste or fear but has consistently favored those who think long-term, act rationally, and embrace uncertainty as part of the game.

Trump Presidency: A New Economic Chapter

I make it a point to avoid diving into political commentary in this blog. My goal is to keep this space neutral, welcoming readers of all perspectives, not creating division. That said, the policies and platforms of any administration inevitably ripple into the economy and, by extension, the investing universe. Let’s examine what a Trump presidency might mean for the economy and markets over this next presidential cycle

Tariffs and Trade Deals

President Trump’s primary platform revolved around implementing tariffs on foreign goods–a strategy that breaks with decades of economic orthodoxy embraced by both Republican and Democratic leaders. Critics argue that tariffs function as a tax on Americans, raising costs for consumers as importers pass on those increases. While this critique has merit, it risks oversimplification. Tariffs are not merely tools to raise prices on foreign goods, but bargaining chips designed to secure better trade deals and incentivize foreign nations to purchase American goods.

Another dimension of the tariff strategy is its potential to bolster American manufacturing. By increasing the costs of imports, domestic alternatives become more attractive. Of course, the viability of this approach varies across industries. For sectors where American manufacturing is prohibitively expensive, tariffs will have little impact. But in industries where the cost differential is narrow, even a slight shift in incentives could bring production back to U.S. soil. The long-term effects of these policies remain uncertain, I think it is too early to tell what the results might be.

Immigration and the Labor Market

Immigration policy is another cornerstone of Trump’s agenda. The debate reached a crescendo in 2024, with Elon Musk and Vivek Ramaswamy defending the H1B visa program against opposition from within their own party. This clash highlights the nuanced interplay between immigration and economic growth. High-skilled immigrant workers contribute significantly to innovation and industry, while broader immigration policies impact labor markets, demographics, and consumption patterns—all of which ripple through the economy.

Trump’s stance on immigration, particularly on curbing illegal entry, aligns with his broader theme of prioritizing American labor and industry. However, the balance between protectionism and the need for a dynamic, skilled workforce remains a key tension that will shape economic policy in 2025 and beyond.

Q4 Performance

As of 1/1/2025, my 10K portfolio was worth $24,761.42 When I started on 8/19/2018, the SPY had a price of $285.06 and my account started with $10,000. As of 1/1/2025 the SPY had a price of $586.08. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation.

| 10K Return(1) | SPY Return(2) | Difference(1-2) | |

| 2018(8/19-12/31) | (13.95) | (13.71) | (.24) |

| 2019 | 37.33 | 32.6 | 4.73 |

| 2020 | 21.22 | 17.59 | 3.63 |

| 2021 | 38.55 | 28.43 | 10.12 |

| 2022 | (27.25) | (18.65) | (8.60) |

| 2023 | 41.36 | 26.72 | 14.64 |

| 2024 | 21.39 | 25.59 | (4.2) |

| Since Inception(8/19/18) | 147.61 | 127.98 | 19.63 |

| CAGR | 15.27 | 13.81 | 1.46 |

Portfolio Performance: Wrapping Up 2024

My portfolio ended 2024 with a bit of a stumble. By the end of the third quarter, I was slightly ahead of the S&P 500, but the fourth quarter erased that lead, leaving me trailing the index by over 4% for the year. Not ideal, but far from cause for alarm. A single year of underperformance is no reason to reconsider one’s strategy—patterns over the long term are what matter most.

Overall, I’m satisfied with how the portfolio has held up. My compound annual growth rate still leads the S&P by nearly 1.5% and sits just under 20% in overall outperformance since inception. Beating the index is no small feat, but I didn’t start this portfolio just to edge out the market. The hope is that this divergence grows meaningfully over time. That said, the index itself has been an exceptional competitor, delivering two consecutive years of 25%+ returns. In such an environment, it’s worth reminding oneself that expectations need to stay grounded. If you’re measuring yourself against perfection, a dose of humility might be in order.

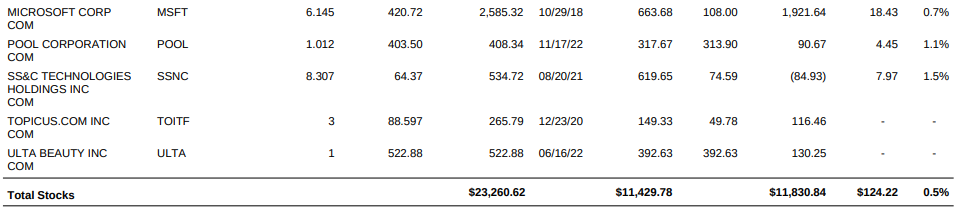

After a busy first three quarters filled with buying and selling activity, the fourth quarter brought a welcome return to stability. I made no portfolio changes, but that doesn’t mean it was uneventful. Businesses are always evolving, and competitive dynamics constantly shift. Let’s dive into how some key holdings fared:

INMD- InMode remains a challenge. The stock continued its downward slide in the fourth quarter, reflecting the stagnation in its growth story. While the company’s fundamentals, particularly its balance sheet, remain impressive, the investment thesis has not played out as hoped. Sitting on $685 million in cash against only $87 million in total liabilities, InMode is in no financial trouble. In fact, it could operate for three years without earning a dime in revenue and still have cash to spare.

This balance sheet gives InMode significant optionality, but the core problem persists: growth has stalled. The company’s reliance on low interest rates has left it vulnerable. Selling high-cost machines to doctors’ offices—a market often reliant on financing—has become a tougher proposition as interest rates remain elevated.

If I were on the board of directors, a role I’ve openly aspired to for any public company, I’d strongly advocate for ramping up R&D spending. InMode’s cash reserves provide ample room to invest in future growth while simultaneously reducing taxable income. Over the past 12 months, the company spent only $14 million on R&D—a figure that could easily be tripled or quadrupled without jeopardizing profitability. Developing new products and diversifying revenue streams would help extend the company’s growth runway and reduce its dependence on economic cycles.

EVO- Evolution had a similarly rough quarter, though the underlying business remains robust. Revenue and margins continue to impress, but regulatory concerns have cast a shadow over the stock. Adding to the turbulence, technical challenges integrating their various platforms have introduced operational headwinds.

The key question is whether Evolution can sustain its current business. Given its extraordinary cash generation and enviable margins, even maintaining the status quo would more than justify the current valuation. If they can navigate regulatory hurdles and deliver even modest growth over the coming decade, the potential for strong returns remains very much on the table.

LULU- Lululemon has been a bright spot. Mid-2024 saw low sentiment around the stock, largely due to Nike’s struggles, which many interpreted as a broader signal of weakness in the athleisure market. Instead, Lululemon has defied expectations, delivering performance.

Revenue and earnings climbed significantly, and the company reduced its share count—a powerful combination under most circumstances. While it’s always tempting to let success breed complacency, Lululemon’s consistent execution in a challenging retail environment is worth celebrating.

Pura Vida!

As always, I would like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Best way to reach me is on Twitter, follow me @TheGarpInvestor.