Happy New Year to all of my esteemed readers and fellow investors! As we usher in 2024, I find myself looking back on a year that was nothing short of an investment rollercoaster. The year 2023 was marked by shifting sentiments and fluctuating market dynamics, yet it culminated in a strong market upturn, boosting spirits and elevating portfolios to impressive heights.

2023 kicked off with a renewed sense of optimism. The shadow of COVID-19 appeared to be fading into the past, making way for a new, vibrant normal. The economy was buzzing, but this rapid growth inevitably stoked the fires of inflation. In response, the Federal Reserve implemented a series of interest rate hikes. These measures, initially perceived as a dampener, ultimately proved effective, curbing the rampant inflation and bringing a semblance of balance to the economic landscape.

The third quarter signaled a turning point in investor sentiment. The Federal Reserve’s efforts, while successful in reining in inflation, might actually have been too potent, casting a shade of apprehension over the economy. The higher interest rates diminished the allure of capital projects. In my own commercial real estate investment business, projects that were attractive at a 3% mortgage rate seemed fraught with risks as rates neared 7%. Across various industries, expansion opportunities dwindled, and for the first time in years, bonds began offering attractive yields, making them a viable alternative to equities.

In the fourth quarter however, we witnessed a dramatic resurgence in the markets. Interest rates appeared to have reached their zenith, sparking a robust recovery in the markets. Consumer confidence, apparently as resilient as ever, played a crucial role in this turnaround. The S&P 500 ended 2023 just a few points shy of its all-time highs.

Looking ahead into 2024, we find ourselves at a crossroads of opportunity and caution. The market’s recent rebound is a beacon of hope, yet it also serves as a reminder of the inherent uncertainties in investing. The coming year promises new challenges as well as opportunities. If interest rates drop back a bit as expected, strategies will shift and so too will markets.

As investors, our focus should be on staying informed, adaptable, and prudent. Diversification, always a key tenet of successful investing, will remain a cornerstone of my strategy. It is essential to balance the pursuit of growth with the wisdom of risk management. That being said, I believe in letting my winners run. I don’t sell a company for being successful, I prefer to let the market reward elite execution.

Here is to a prosperous 2024. Let’s approach our investment decisions with a blend of optimism, diligence, and a keen eye on changing market dynamics. I wish you all a wonderful year and continued success in all financial endeavors!

Q4 Performance

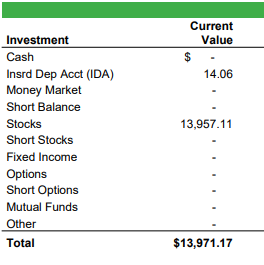

As of 1/1/2024, my 10K portfolio was worth $20,398.32. When I started on 8/19/18, the SPY had a price of $285.06 and my account started with $10,000. As of 1/1/2024 the SPY had a price of $475.31. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation.

| 10K Return(1) | SPY Return(2) | Difference(1-2) | |

| 2018(8/19-12/31) | (13.95) | (13.71) | (.24) |

| 2019 | 37.33 | 32.6 | 4.73 |

| 2020 | 21.22 | 17.59 | 3.63 |

| 2021 | 38.55 | 28.43 | 10.12 |

| 2022 | (27.25) | (18.65) | (8.60) |

| 2023 | 41.36 | 26.72 | 14.64 |

| Since Inception(8/19/18) | 103.98 | 82.55 | 21.43 |

| CAGR | 14.22 | 11.88 | 2.34 |

Reflecting on 2023, I am excited by the success we’ve witnessed, both in the broader market and within my own portfolio. My portfolio’s performance this year has been nothing short of extraordinary, surpassing the SPY by nearly 15%, with a 21.43% outperformance since inception. While such remarkable returns are not something I count on repeating indefinitely, I would certainly welcome them with open arms should they occur. However, it’s wise to remember, as Warren Buffett often reminds us, “The stock market is designed to transfer money from the Active to the Patient.”

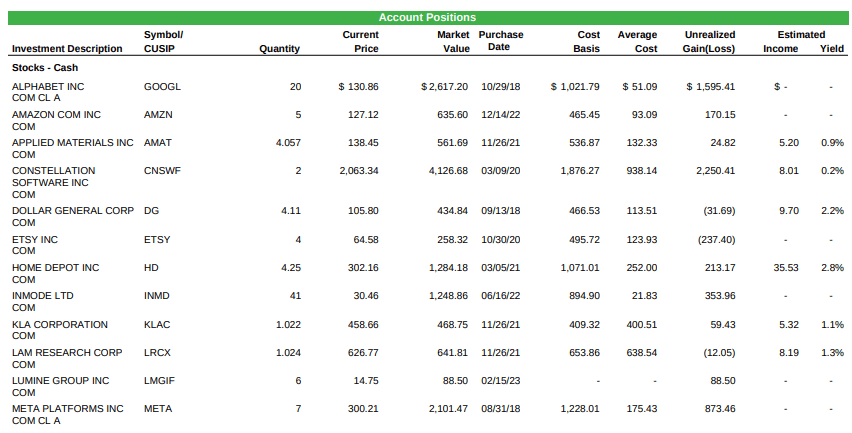

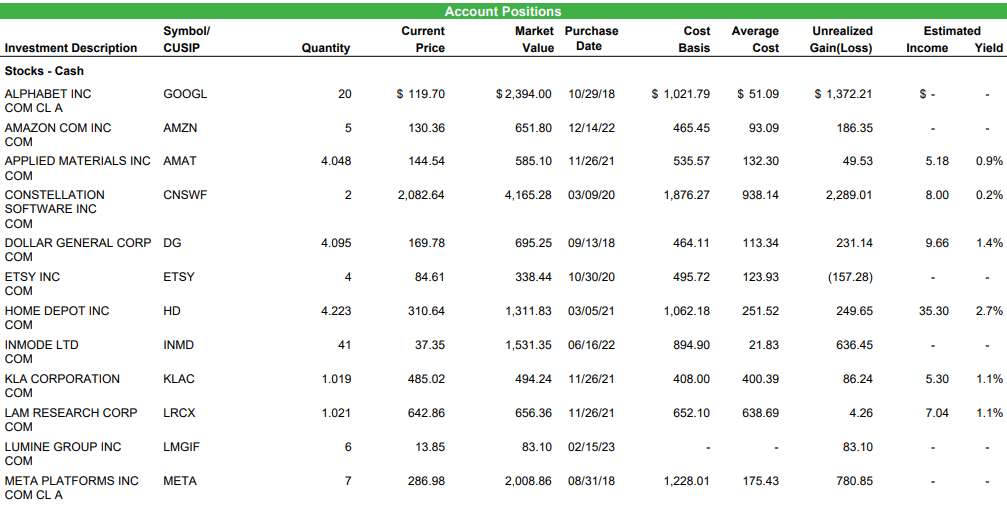

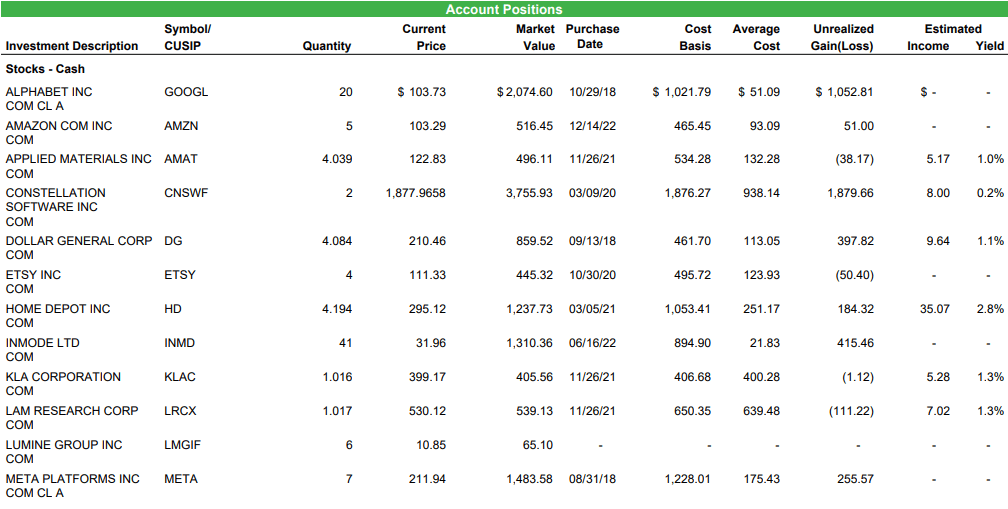

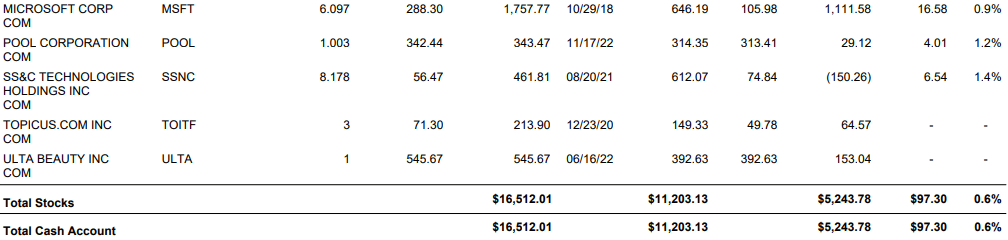

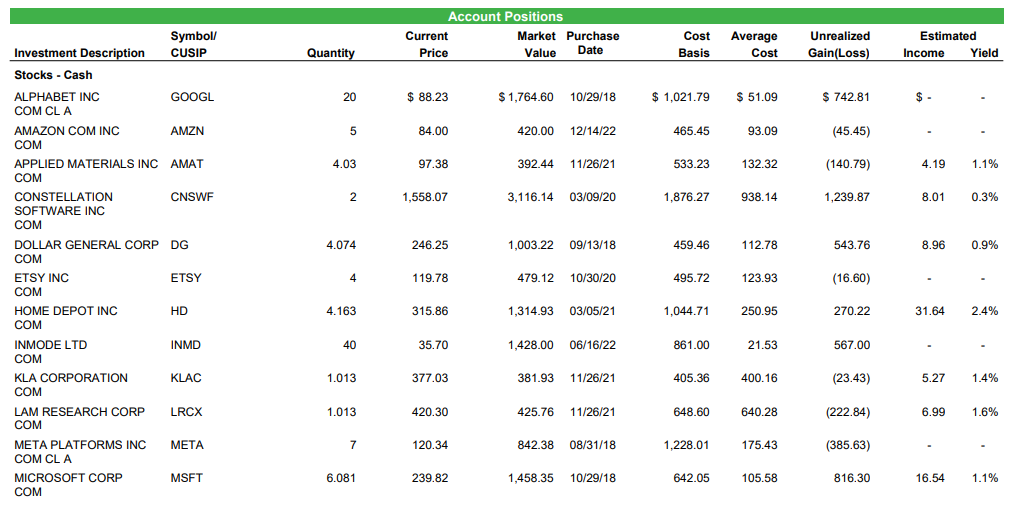

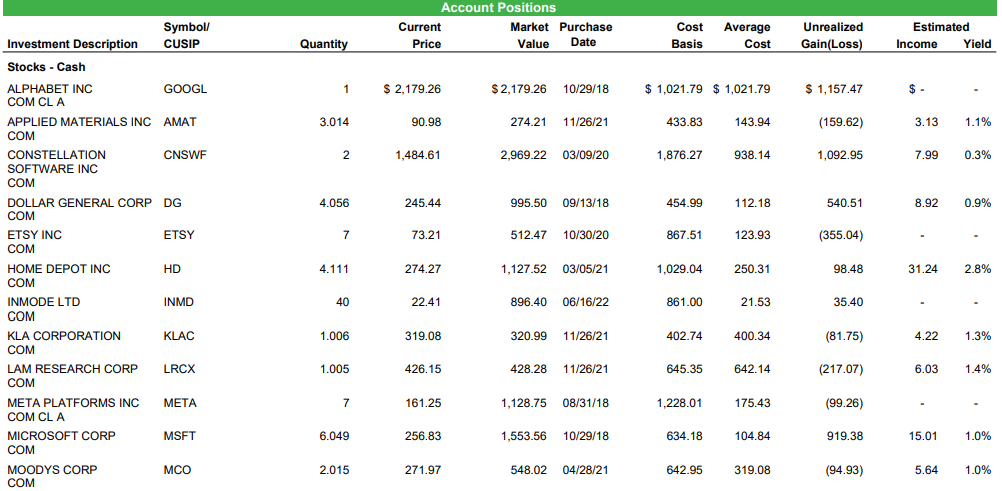

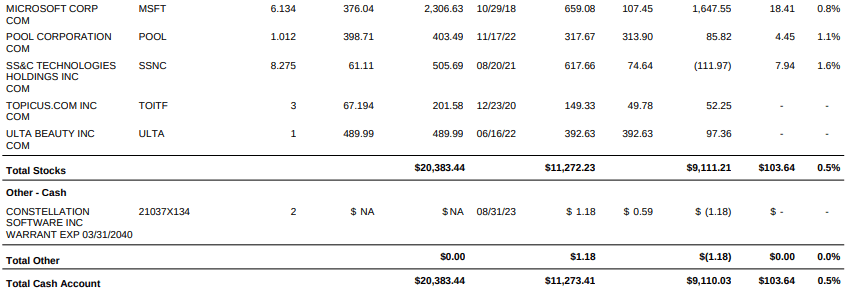

This year, mega-cap technology stocks have been the standout performers, just as they have been the trailing decade. My investments in this sector, GOOG, AMZN, MSFT, META, have borne significant fruits, contributing substantially to the portfolio’s impressive growth. Constellation Software now constitutes nearly a quarter of my total portfolio. Conventional Wall Street wisdom might suggest a rebalancing strategy, redistributing assets to reduce concentration. Yet, I disregard such recommendations. The ascent in the stock is a testament to the performance of the underlying business. While some may argue the valuation is stretched, I am prepared to embrace any temporary pullbacks as part of the journey. I’m not betting on the next year, but on what will be 5, 10, and 20 years down the line.

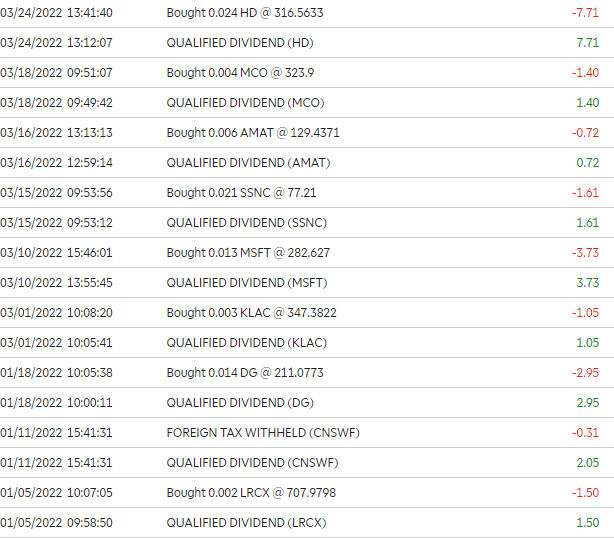

This past quarter has continued in the same vein as previous ones, with no transactions in my portfolio. This steadfast approach may not be the most exhilarating, but it is the tactic that works for me. By investing in top-tier businesses globally, I place the growth of my investments in the hands of those who know their companies best – the operators.

However, even the most carefully curated portfolio encounters challenges. A few stocks in my holdings have raised concerns, not due to a dip in their share prices, but rather because of their business performance. Dollar General, for instance, has been a particular laggard. The company seems to have hit a plateau in revenue growth, and its margins are facing increasing pressure. Additionally, the rising interest rates have started to weigh on the balance sheet, with growing interest expenses affecting profitability.

The decision making process in such scenarios is intricate. If Dollar General’s stock had remained stable while the business fundamentals deteriorated, the choice to sell would be straightforward. The stock however has mirrored the company’s declining business performance, making the decision more complex.

In my past experiences, I’ve learned that acting too hastily when a solid business encounters temporary setbacks can be premature. Allowing a company time to demonstrate its resilience is often a wise strategy. The critical task is to discern whether the issues faced are short-term hurdles or indicative of a longer-term decline. This judgment is where astute analysis becomes invaluable, distinguishing a reactionary decision from a strategic one.

With that I’d like to once again wish you all a happy new year. I would also like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Best way to reach me is on Twitter/X, follow me @TheGarpInvestor