The third quarter of 2025 will be remembered for one thing: the market’s refusal to quit.

Every time it looked ready to correct, it found a way to climb higher. A dip on Monday became a rally by Friday. The bears growled, the bulls shrugged, and the indices marched to new all-time highs. It was the type of market that made skeptics look foolish, and optimists look prescient.

Semiconductors and AI once again led the charge. The spending spree in artificial intelligence is unlike anything we’ve seen in decades; a corporate arms race funded not by speculation, but by companies drowning in cash. Every major tech firm is building data centers the size of small cities, and Wall Street can’t decide whether to call it the next industrial revolution or a bubble prophesied to tank the entire economy.

Frankly, I don’t know which it is either. There’s something surreal about watching hundreds of billions flow into AI infrastructure, but when the money is coming from balance sheets bursting with cash, it’s hard to call it reckless. When you’re minting $20–$30 billion in free cash flow every quarter, you have to spend it somewhere. And right now, AI is the only story worth telling. With valuations already stretched, share buybacks offer meager yield by comparison.

Elsewhere, inflation cooled slightly, yields eased, and talk of rate cuts returned to the conversation. Investors are once again dreaming of a soft landing, and for now, the dream seems intact.

Still, there’s a quiet tension beneath the euphoria. When everyone’s on one side of the trade, history has a way of humbling the crowd.

The Industrial Hangover

Beneath the surface of market euphoria, the real economy looked tired.

Freight and industrial activity continued to lag, showing none of the exuberance seen in tech. Truckload volumes remained weak, pricing stayed soft, and carriers kept exiting the market. Trucking is a bellwether for the broader economy, so when truckers suffer, it is rarely a good omen.

Manufacturing data told a similar story. New orders cooled, backlogs thinned, and companies quietly pushed out CapEx plans. The industrial engine of the economy is idling, even as markets behave like we’re in a boom.

AI and semiconductors can only levitate the indexes for so long. Eventually, for the economy to hum, there needs to be goods to move. And right now, the people who actually move them are still waiting for the recovery to arrive.

In Memory of My Father

This quarter wasn’t just about markets, it was about loss. Unfortunately, my father passed away in mid-August, and life hasn’t been the same since.

He taught me everything I know, about business, yes, but more importantly about life. How to think independently, act with integrity, and treat people with respect. To him, every action was personal and every moment a lesson. He believed in fairness, in treating others the way his own immigrant parents would have wanted to be treated. That philosophy shaped not just the way I work, but the way I try to live.

My dad was the reason I got into business and investing. He’s the reason I never had to get a “real” job, bringing me into the family business right after college. That gave me the freedom to study the greats: Buffett, Munger, Graham, and Fisher. To build my own investing philosophy. Without his support, guidance, and belief, nothing I do today would have been possible.

But more than that, he’s the reason I care about doing it the right way. He had a deep sense of honor that guided everything he did. He believed business should be tough but decent, that success meant nothing if it wasn’t shared with those less fortunate. He never cared much for appearances or praise; he just wanted to build something lasting and to take care of those around him.

Losing him has been devastating. There’s an emptiness in my days that I don’t think will ever fully fade. But even through the grief, I can feel his presence, in the way I approach a problem, in how I weigh a risk, in the quiet reminder to do things with integrity.

He built more than a business; he built a foundation. One strong enough for his family to stand on long after he was gone. My goal now is simple: to keep building on what he started, with the same integrity, patience, and determination that defined his life.

Q3 Performance

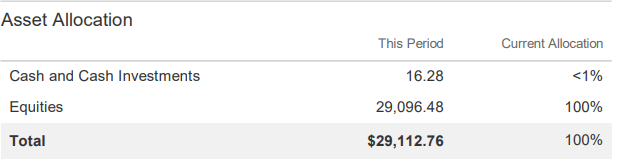

As of 10/1/2025, my 10K portfolio was worth $29,112.76. When I started on 8/19/2018, the SPY had a price of $285.06 and my account started with $10,000. As of 10/1/2025 the SPY had a price of $668.45. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation.

| Year | 10K Portfolio | SPY | Outperformance |

|---|---|---|---|

| 2018 (8/19–12/31) | -13.95% | -13.71% | -0.24% |

| 2019 | 37.33% | 32.60% | 4.73% |

| 2020 | 21.22% | 17.59% | 3.63% |

| 2021 | 38.55% | 28.43% | 10.12% |

| 2022 | -27.25% | -18.65% | -8.60% |

| 2023 | 41.36% | 26.72% | 14.64% |

| 2024 | 21.39% | 25.59% | -4.20% |

| 2025 (1/1–3/31) | -5.03% | -3.76% | -1.27% |

| 2025 (4/1–6/30) | 19.11% | 10.43% | 8.68% |

| 2025 (7/1–9/30) | 3.93% | 8.52% | -4.59% |

| Since Inception (8/19/18) | 191.12% | 162.30% | 28.82% |

| CAGR | 16.10% | 14.50% | 1.60% |

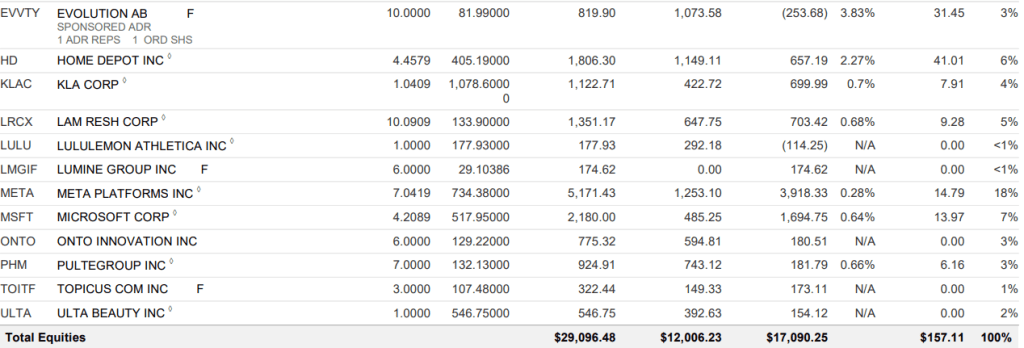

Quarter three was solid overall, but I trailed the broader market. While the major indexes marched higher, my portfolio moved at a slower pace. A couple of names drove nearly all the results, one on the way up, the other on the way down.

On the bright side, Alphabet (GOOGL) was a star performer. It began the quarter at $176.23 and closed at $243.10, a gain of nearly 38%. For a company of that size, such a move in a single quarter is remarkable. What changed wasn’t the business, it was sentiment. In the spring, investors feared AI might erode Google’s dominance; by late summer, they were convinced it would strengthen it. As usual, the truth probably lies somewhere in between. Alphabet remains an extraordinary company, cash-rich, dominant, and still early in monetizing its AI potential.

On the other side of the ledger was Constellation Software, my largest holding. Constellation dropped from $3,670 to $2,714 a share, a 26% reduction.

In response to growing investor questions, management held a webcast to address how AI could affect their business. Their tone was measured, cautiously optimistic. They acknowledged that AI could reshape parts of the vertical market software industry, but also emphasized opportunities to integrate it within their own products to enhance functionality and efficiency.

In my view, the real long-term threat isn’t customers replacing Constellation’s software with in-house tools. It is from competitors utilizing AI to create cheaper alternatives, compressing pricing power. That risk remains theoretical today, but over the next decade, it could emerge more clearly. For now, the company’s deep customer relationships, decentralized structure, and disciplined acquisition strategy remain intact.

Then came the tougher news: on September 25th, founder and CEO Mark Leonard stepped down immediately due to health reasons. Details were limited, but the situation sounded serious. I wish him a full and speedy recovery.

Operationally, little should change. Constellation remains famously decentralized, with capital allocation delegated to hundreds of individual managers. But what the company will miss is Leonard’s quiet wisdom. He had a rare blend of rationality, restraint, and long-term discipline. He built a culture that prized shareholder alignment and focused relentlessly on achieving high hurdle rates.

Constellation’s next chapter will test whether that culture endures without its architect. My bet is that it will, because the best systems, like the best investments, are built to outlast their founders.

I’m far from the first to notice that Leonard and Buffett stepped down in the same year, but I owe both men a debt of gratitude. Together they’ve shaped my investment philosophy more than anyone else. Each rejected the noise of the moment and instead built patiently for the decades ahead. They rewarded shareholders and turned compounding into an artform. Buffett’s eventual retirement was inevitable, but Leonard’s came as a shock. Still, Constellation will carry on, and every future result will trace directly back to the framework he built.