The first quarter of 2025 was a test of patience. It wasn’t dramatic, but it was draining. Markets didn’t crash, they just quietly slid lower, day after day, until doubt began to mount in investors’ confidence. There was no headline moment, just a slow erosion of optimism.

Then, just as the quarter ended, everything changed.

New tariff threats and a sudden shift in political rhetoric out of Washington threw gasoline on a smoldering market. Volatility surged. It felt like being tossed around in the open sea with no life raft to reach out to.

This isn’t normal. But it’s not unprecedented either. Markets often move this way: long periods of calm followed by sharp, confusing bursts of chaos. These swings are drastic, but conventional investing wisdom tells us to be brave. In fact, it is likely the most important thing an investor can do. What is that action we can all take to protect our portfolios? Nothing. It feels like we need to act, do something, counteract the downward momentum. But history has been clear: panic selling is the fastest way to destroy wealth.

Warren Buffett has often said that the stock market is designed to transfer money from the active to the patient. The greatest action you can take in moments like these is to stay invested. Even better, keep buying. Keep adding with each paycheck and let time do the heavy lifting.

Tariffs

Trump’s tariff announcements landed like a thunderclap. For months, markets had been pricing in a “business as usual” political environment. Then came talk of sweeping tariffs 10%, 25%, 60%, 90% maybe even more on certain countries and items, and suddenly the calm was gone.

Markets hate uncertainty. But they really hate abrupt, hard to quantify change. And that’s exactly what sweeping tariffs bring. Sudden cost increases ripple through supply chains, pricing models get upended, and companies are left scrambling to adjust. The result? Margin pressure, inflation concerns, and a wave of investor unease.

To be clear, there’s a certain logic to Trump’s strategy. He wants the Federal Reserve to cut rates, weaken the dollar, and ultimately make U.S. debt easier to refinance. But even if he is correct and tariffs lead to a major uptick in American manufacturing, better trade deals and lower prices for the American people, the way he went about it is ridiculous. There’s no nuance, no predictability, just a tweet here, a threat there, and a market left to pick up the pieces.

AI CapEx

While headlines scream about tariffs and inflation, one of the most important investment stories of 2025 is happening quietly in server farms and substations.

We’re in the middle of an AI infrastructure boom, something akin to the railroads in the 1800s or broadband in the 2000s. The biggest companies in the world: Microsoft, Amazon, Google, Meta, are spending tens of billions to build the physical backbone of AI. That means more chips, more power infrastructure, and more data centers.

AI may still feel like a buzzword to many, but the capital being deployed is very real. If you’re a long-term investor, this is an investment you want exposure to. But picking the winners will be hard, frankly I have no idea who will ultimately be the winners 10 years from now. Therefore, there are a few different ways to get that exposure. You can get exposure through broad market ETFs, or more targeted ones focused on semiconductors or data centers.

Capital Discipline

In uncertain times, investors don’t need excitement, they need reliability. With markets whipsawing on headlines and political posturing, there’s comfort in companies that keep things simple: generate cash, reinvest prudently, and return the rest to shareholders. These aren’t the loudest businesses in the market, but they tend to be the ones you can sleep well owning.

Capital discipline doesn’t mean stagnation, it means focus. Companies with strong balance sheets and consistent buybacks or dividends offer something rare right now: predictability. When so much feels out of control, owning businesses that know how to allocate capital wisely is one of the few defenses you have. No need to guess the next macro turn when your portfolio is built on steady compounding.

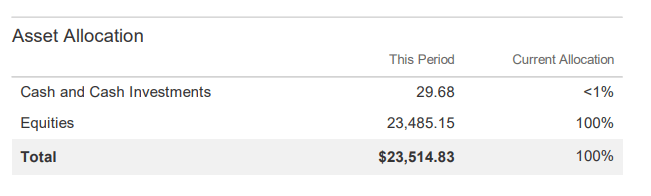

Q1 Performance

As of 4/1/2025, my 10K portfolio was worth $23,514.83 When I started on 8/19/2018, the SPY had a price of $285.06 and my account started with $10,000. As of 4/1/2025 the SPY had a price of $560.97. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation.

| Year | 10K Portfolio | SPY | Outperformance |

|---|---|---|---|

| 2018 (8/19–12/31) | -13.95% | -13.71% | -0.24% |

| 2019 | 37.33% | 32.60% | 4.73% |

| 2020 | 21.22% | 17.59% | 3.63% |

| 2021 | 38.55% | 28.43% | 10.12% |

| 2022 | -27.25% | -18.65% | -8.60% |

| 2023 | 41.36% | 26.72% | 14.64% |

| 2024 | 21.39% | 25.59% | -4.20% |

| 2025 (1/1–3/31) | -5.03% | -3.76% | -1.27% |

| Since Inception (8/19/18) | 133.51% | 118.87% | 14.64% |

| CAGR | 13.80% | 12.56% | 1.24% |

I underperformed the index in the first quarter, tightening what had previously been a solid margin of outperformance. I’m still ahead overall, but my CAGR lead has narrowed to just 1.24% gap that could vanish with a few bad days. That’s investing. Progress often comes in zigzags. Still, I remain confident in the businesses I own. Not blindly, but with risk-adjusted conviction based on how they’re actually performing, not just how the stock happens to trade.

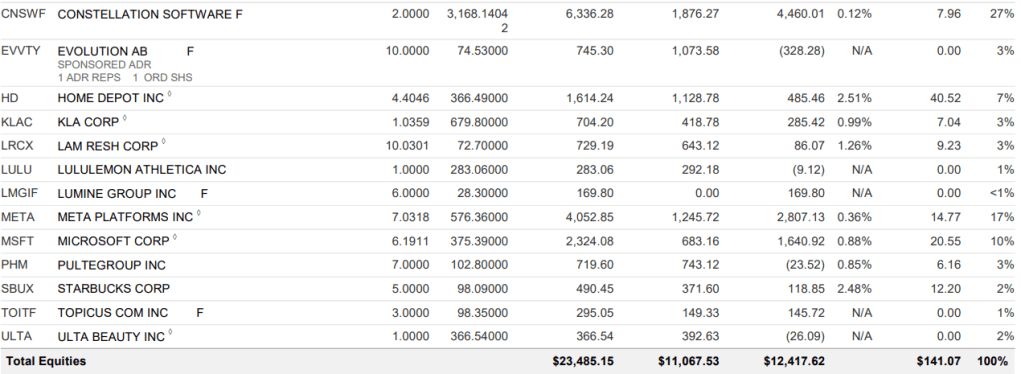

INMD- In mid-March, I finally sold my position in InMode. It’s tough to watch a company consistently underdeliver. I’m not concerned with daily stock moves, but I care deeply about business performance, and InMode’s kept heading in the wrong direction. The continued stock decline was no mystery; it was a reflection of weakening fundamentals.

Their business model is particularly sensitive to interest rates. InMode sells high-ticket medical devices, and most of their customers, small clinics and doctors’ offices, finance those purchases. As borrowing costs soared, the ROI on that equipment shrank. What was once a no-brainer purchase became a tough sell. Add potential tariff pressure on top, and the near-term outlook looks cloudy.

If rates return to more attractive levels, I’d absolutely revisit the name. InMode still has a strong model under the right conditions, but for now, the environment is stacked against them.

PHM- This quarter, I initiated a new position in PulteGroup, a homebuilder that, in my view, stands apart in an industry not known for its discipline.

Homebuilding can be a brutal business. It’s cyclical, capital-intensive, and sensitive to rates, labor, and materials. But what drew me to Pulte is how they’ve built a business that respects those realities rather than fighting them. They don’t chase volume. They don’t overextend. They allocate capital with care, prioritize returns on equity, and run a tighter operation than most in the space.

Pulte leans heavily on spec home construction, which shortens build cycles and improves cost control. Albeit, that does introduce some risk, they could be stuck with inventory if demand cools, but Pulte mitigates it by focusing on buyer segments less sensitive to rates, like move-up buyers and retirees. Combine that with a conservative balance sheet and consistent share buybacks, and you get a business that compounds value even when the housing market isn’t on fire.

This isn’t a bet on housing roaring back. It’s a bet that Pulte, even in an average housing environment, can quietly outperform thanks to its operational rigor and capital stewardship. That’s the kind of company I’m comfortable owning for the long haul.

As always, I would like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Best way to reach me is on Twitter, follow me @TheGarpInvestor.