It’s been an eventful third quarter here in 2024. With an election just around the corner, it seems as though every news outlet is gearing up for what they’re calling a decisive moment in history. As usual, we’re told that if the other side wins, it’s the end of America as we know it. Well, here’s a little context: since 1789, we’ve had 46 different presidencies–Democrat, Republican, and even a few Whigs and Federalists thrown into the mix.

Yet, through each one of these administrations, America has persisted. The stock market, which is sitting at all-time highs today, didn’t get there by luck. It’s a reflection of ever-increasing productivity and the ingenuity of American businesses. Despite the noise, the fundamentals remain strong, and by almost any measure, life is better today than at any other time in human history.

Now, I’m not blind to the challenges that lie ahead. Our country will face its share of obstacles in both the near and distant future. Illegal immigration, inflation, a crisis in the Middle East, climate change—these are all very real and important issues just to name a few. But no matter who sits in the Oval Office, things have a way of working themselves out. We can sit around mulling over doomsday scenarios, but that doesn’t really get us anywhere.

Whether the White House belongs to Trump or Harris next year, my investment advice remains the same: invest in quality businesses that earn high returns on invested capital. If picking individual stocks is too hard— and for most, it is not even worth attempting– a diversified selection of low-cost index funds will do just fine. Stick to a sensible plan, avoid the temptation to react to short-term noise, and keep investing steadily over your lifetime. Do that, and the odds of success are overwhelmingly in your favor.

Hurricanes

I’m writing this after yet another major hurricane hit Florida, with Hurricane Milton having made landfall. Thankfully, the damage and loss of life were less severe than feared, but storms of this magnitude are always tragic events. Insurance companies, as usual, will bear the brunt of the financial burden. It will likely take years for claims to be fully settled, and we can expect to see local and regional insurers pushed to the brink, if not into outright bankruptcy. Even some of the world’s largest reinsurers will likely feel the impact.

What’s next for Florida? That’s a tough question. If I were running a major insurance firm, I’d think long and hard before writing any new policies in the state. The risks are simply too high and unpredictable. Insurers are faced with a difficult choice: either pull out of the market entirely, leaving homeowners stranded, or raise premiums to levels that make owning a home unaffordable for most families. Neither option is appealing, and neither bodes well for the future of Florida. And that’s just looking at the residential side. The commercial insurance market, which is critical for businesses, faces its own set of challenges and could be hit just as hard.

The issue is far from simple, and frankly, its one I’m glad I don’t have to solve. It’s going to require a combination of government intervention and innovative solutions from the private sector to keep the state insurable. It’s not an easy fix, but it’s necessary. In the meantime, I wouldn’t fault any insurer for pulling back. Sometimes, when the odds are stacked against you, the smartest move is to walk away.

Port Strike

A big storyline that flew somewhat under the radar was the East Coast port strike. There was some media coverage, sure, but I don’t think the public truly grasped just how close we came to economic calamity. Thankfully, cooler heads prevailed, and they reached an agreement within 72 hours of the strike beginning. But make no mistake–this could have been a far bigger story. If the ports had been shut down for any significant length of time, the repercussions would have rippled throughout the entire U.S economy.

Think of the ports as arteries of commerce. A shutdown in port activity doesn’t just impact hte coasts–it brings the entire logistics system to a standstill, creating a logjam that clogs up everything from shipping to trucking to rail. And when the gears of the economy grind to a halt, everyone–from the largest manufacturers to the corner grocery store, feels the squeeze.

We should all be breathing a huge sigh of relief that a deal was struck, and the prots are back in operation. It’s a reminder of just how fragile and interconnected our economic systems really are. When one piece of the puzzle goes missing, it doesn’t take long before the whole picture starts to blur.

Q3 Performance

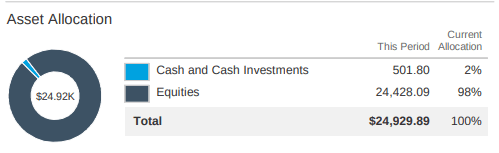

As of 10/1/2024, my 10K portfolio was worth $24,929.89 When I started on 8/19/2018, the SPY had a price of $285.06 and my account started with $10,000. As of 10/1/2024 the SPY had a price of $568.62. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation.

| 10K Return(1) | SPY Return(2) | Difference(1-2) | |

| 2018(8/19-12/31) | (13.95) | (13.71) | (.24) |

| 2019 | 37.33 | 32.6 | 4.73 |

| 2020 | 21.22 | 17.59 | 3.63 |

| 2021 | 38.55 | 28.43 | 10.12 |

| 2022 | (27.25) | (18.65) | (8.60) |

| 2023 | 41.36 | 26.72 | 14.64 |

| 2024(1/1-9/30) | 22.21 | 21.38 | .83 |

| Since Inception(8/19/18) | 149.29 | 112.29 | 37 |

| CAGR | 16.10 | 13.09 | 3.01 |

The third quarter saw only a small change in my portfolio performance. This quarter, my portfolio continued to closely mirror the index, achieving only a marginal outperformance in comparison. It is vital to acknowledge, however, that a tiny outperformance will lead to large differentials over time. I continue to be satisfied with the portfolio’s execution in both actual and relative terms. If you had told that this portfolio would compound at a 16.1% CAGR when I first started this blog, I would never have believed you, but here we are.

2023 saw few, if any, changes to my portfolio. 2024 however has been uncharacteristically busy for me, particularly in this past quarter. I generally recommend not making too many adjustments to your portfolio once it is constructed. I am often an advocate for the “coffee can portfolio” strategy–a long term, buy and hold approach where you set aside funds in a metaphorical coffee can, remaining untouched for decades. But sometimes I think activity is necessary. Quality remains paramount, and when companies no longer meet our high standards, they must be replaced with superior alternatives.

Transactions

SBUX- Starbucks is a name that needs no introduction. People are addicted to coffee and no one does it better than Starbucks. Under CEO Laxman Narasimhan Starbucks experienced some challenging times. Drink prices had climbed too high, and competition began to eat into its market share, particularly in China, which was supposed to be a key growth driver. Narasimhan appeared to be in over his head, and he struggled to provide effective solutions. His now infamous interview with Jim Cramer left viewers shaking their heads, as he talked about “providing value to customers” without offering any actionable steps.

In early July, I saw a dip in the price and felt it presented a good opportunity to accumulate shares. Starbucks is a brand with immense staying power, and I believed the challenges it faced were temporary. Even with a subpar CEO, the underlying strength of the brand made it a worthwhile investment. I was betting that a focus on brand protection would lead to long term success and strong returns.

Well so far, my purchase has done extremely well. I had no inkling that Narasimhan would be fired and replaced by Brian Niccol, but I’m certainly pleased with the outcome. Niccol is a restaurant industry veteran, having previously led Taco Bell and Chipotle to impressive heights. Wall Street is confident that he can do the same with Starbucks, as the stock has surged since his appointment. Has the stock gotten a bit ahead of itself? Probably, but I’m in it for the long haul, and these short-term price movements don’t concern me.

POOL- Now it’s time to confess one of my portfolio’s biggest mistakes. I sold out of Pool Corp shortly after buying Starbucks. Why did I sell? The easiest answer is that I’m an idiot. In all seriousness, I sold due to what I perceived as declining business fundamentals. Revenue in 2023 began to fall, and that trend has continued into 2024. The pool industries going through a rough patch, as many people who wanted a pool installed one during the pandemic, pulling forward years of demand.

The maintenance side of the business is still performing well, as all those newly built pools now need constant upkeep. This is a great source of recurring, high margin revenue. However, overall sales have dipped.

In hindsight, selling appears to have been a clear error. Pool Corp’s stock is up more than 20% since I exited. I try not to check the price too often, as it’s just a painful reminder. Pool Corp remains a tremendous business, and it dominates its sector. I simply believed I had better opportunities elsewhere. So far, that bet hasn’t paid off.

LULU- Lululemon has always been a name associated with premium quality, and for years, it commanded a premium valuation. Until recently, it was nearly impossible to buy this brand at a reasonable price. However, recent challenges have caused the stock to take a tumble, offering what may be the first real opportunity in the company’s history for long term investors to buy at an attractive valuation.

The issues behind the price drop are mainly related to concerns about slowing growth and increased competition. We saw a disappointing quarter from Nike, indicating that apparel and footwear sales are likely to be challenged as rising prices squeeze consumers’ budgets. Despite these headwinds, I believe this has provided an opportunity. Lululemon’s brand equity, loyal customer base, and unique product offerings make it a compelling buy at current levels.

At a fundamental level, Lululemon is a very good business. If you can sell a pair of yoga pants for $100, it’s hard not to generate strong margins. Lululemon boasts nearly 60% gross margins and close to 25% operating margins. For reference, both Nike and Under Armour have gross margins that hover around 45% with operating margins of 12.5% and 4% respectively. That means for every dollar of sales, Lululemon makes double the operating income of Nike and six times that of Under Armour, a testament to its status as a true premium brand.

Growth has also been stellar over the years. In 2016, Lululemon had less than half the sales of UA. Today their sales are nearly double those of UA. Perhaps that is more indicative of UA’s decline than Lulu’s ascendence, but in that same time period Lulu increased sales by almost five times, which for any company is pretty incredible.

In summary, Lululemon’s stock price decline presents a rare opportunity. While the short term may be rocky, the long term outlook for this brand remains bright, as it continues to occupy a unique position in the market. It is a classic example of being able to buy a great business at a fair price, and that’s exactly the kind of opportunity I like to take advantage of.

ETSY- I finally decided to liquidate my holdings in Etsy. Since I initially trimmed the position in 2022, the company’s performance has continued to disappoint. Revenue has flatlined, and Etsy has struggled to find new growth avenues. Has the market simply reached saturation? Or has management failed to connect the right products with the right consumers? Time will tell.

More concerning, however, has been their capital allocation. Etsy made multiple acquisitions at inflated prices and spent on share buybacks at overvalued levels. Capital allocation is critical in any business, and Etsy’s missteps in this area were a major red flag. Unfortunately, I was correct when I first trimmed my position, but I should have sold out entirely. I ended up selling my remaining shares at a 50% lower price than my initial sale. Still, it wasn’t all bad news, as the stock has fallen another 20% since I exited. I’ll root for Etsy in the future, but it will no longer be a part of my portfolio.

As always, I would like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Best way to reach me is on Twitter, follow me @TheGarpInvestor.