The 2024 stock market continues to surprise, with major indices such as the S&P 500, Nasdaq, and Dow Jones Industrial Average reaching new all-time highs. While valuations continue to stretch, it is hard to determine whether such valuations are appropriate. Although CPI numbers show inflation has cooled, prices are still significantly elevated from years prior. Just compare your current grocery bills to those from five years ago; the change is striking. Despite prognosticator expectations for a market pullback, markets continue to soar. They follow no set path, driven instead by the whims of buyers.

S&P 500 concentration

A notable trend in 2024 is the increasing concentration within the S&P 500, where the top companies dominate more than ever. This has been a long term multi-year trend, but 2024 has seen an intense uptick in consolidation.

From this CNBC article.

This concentration is not inherently good nor bad, but is merely a statement of fact. Concentration is inherently baked into capitalism’s core: capital begets more capital.

These top 10 names are highly valued, but often deservedly so. They are the best companies in the world, growing faster than the average S&P 500 company, with higher returns on invested capital and cleaner balance sheets. Their success is no coincidence; they are fantastic companies run by the world’s best managers.

However, this concentration does put the market at risk, much like it would a portfolio so heavily concentrated. A significant move in any of these top names will disproportionately impact markets. Should any of these companies fail to sustain their exceptional performance, the resulting fall could be swift, dragging markets down with it. Will that happen? I have no idea, but we all should be aware of the risk.

Opportunities Beyond the Top 10

This extreme concentration has actually hidden much of the damage seen elsewhere in the index. While the top companies’ stocks have lifted markets, many other notable names are at or near 52-week lows. Large well-known quality companies like Starbucks, Lululemon, and Comcast have been significantly impacted.

This situation presents what I believe to be an opportunity for those willing to focus on fundamentals. This is a time to find great companies trading at discount prices. With careful analysis, discerning investors can capitalize on this moment, potentially reaping substantial rewards in the long term.

Comparison of NVDA to Cisco in 2000

I want to comment quickly on a prevailing narrative I often see. NVIDIA has, of course, been the market’s top performer and deservedly so. I have never in all my years observing the market and following company financials seen a company execute so well. They are increasing revenues, profits, and free cash flow at rates that are unheard of for massive companies. To say that it is impressive, would fail to convey just how amazing their results have been.

Many pontificate that NVIDIA is a bubble, just waiting for the rug to be pulled out from under them. They compare NVIDIA to Cisco in 2000 right before the dot-com crash. For those unaware, Cisco was the market darling before the crash. They were a high performer, but ended up trading to such a ludicrous multiple, that business results couldn’t possibly make it worth it. They reached a price of $69 in 2000, which turned out to be such a wild price, that now, in 2024, they have still yet to reach back to those lofty heights. Meaning that if you had purchased Cisco stock in 2000 and held your shares, you still would have a negative return even 24 years later.

Meanwhile, an investment into the S&P 500 at the same time, would have nearly quadrupled over the same period. Given NVIDIA’s rapid rise, I understand the comparison, but let’s take a look at some numbers so we can really compare.

Here is a snapshot from Cisco’s 2000 annual report, showing their financial results.

Cisco’s business results were undeniably good. Sales and net income both grew at high rates. Sales were up over 50% in 2000 and net income was up over 30%. They did however issue a significant amount of shares, meaning earnings per share did not rise nearly as fast.

Now let’s look at NVIDIA’s results from this past quarter.

I frankly see no real comparison here. NVIDIA is a vastly better business, growing revenue 5 times as fast as Cisco was in 2000 and growing earnings over 10 times as fast. On a per share basis, it isn’t even worth discussing. Cisco grew EPS at 24% in 2000, NVIDIA was up 461% year over year.

With these kinds of growth rates, it is almost impossible to value NVIDIA too high. If they can keep up even some of this trajectory, almost any price is justified. Now of course the obvious question is how big can they get? Their revenue is driven by other megacap tech stocks AI spending. How high can that spending go? I have no idea. Additionally, you can be certain that every company in the AI arena is gunning for NVIDIA. Intel, AMD, and every other chipmaker are dying to capture some of that business and they will do everything in their power to make it happen. Can they catch up? Probably not anytime soon, but maybe. Apple, Amazon, Meta and so on are all also working on designing and building chips in house. They all see how much money NVIDIA is making, so if they have an opportunity to cut them out of the loop and keep that profit in house, they will do so. The returns are simply too high to let NVIDIA continue unopposed.

For those reasons, I have stayed away from the stock. I am unable to answer any of these questions, but I have assuredly looked on in envy. I have no clue as to where NVIDIA’s business goes from here. Perhaps NVIDIA’s next 24 years will be no better than Cisco’s last 24, but I wouldn’t want to bet against Jensen Huang and did want to point out that it is a rather lazy and poor comparison.

Q2 Performance

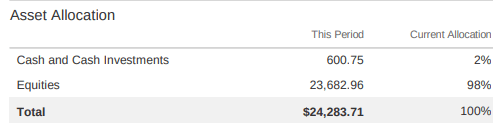

As of 7/1/2024, my 10K portfolio was worth $24,283.71. When I started on 8/19/2018, the SPY had a price of $285.06 and my account started with $10,000. As of 7/1/2024 the SPY had a price of $545.34. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation.

| 10K Return(1) | SPY Return(2) | Difference(1-2) | |

| 2018(8/19-12/31) | (13.95) | (13.71) | (.24) |

| 2019 | 37.33 | 32.6 | 4.73 |

| 2020 | 21.22 | 17.59 | 3.63 |

| 2021 | 38.55 | 28.43 | 10.12 |

| 2022 | (27.25) | (18.65) | (8.60) |

| 2023 | 41.36 | 26.72 | 14.64 |

| 2024(1/1-6/30) | 19.05 | 16.11 | 2.94 |

| Since Inception(8/19/18) | 142.84 | 110.79 | 32.05 |

| CAGR | 16.31 | 13.55 | 2.76 |

2024 has sustained the positive momentum of my portfolio, both in absolute terms and relative to the SPY. Since its inception, my portfolio has outperformed the SPY by an impressive 32%. This significant outperformance can be attributed to a compounded annual outperformance of 2.76%. It’s a testament to the power of consistent, incremental gains held over extended periods, which can culminate in substantial differences.

Transition To Charles Schwab

You may notice a change in my portfolio’s presentation format, this is due to my recent tradition to Charles Schwab. This change was not voluntary; I originally used TD Ameritrade as my brokerage, but they were acquired by Schwab. The integration took place a couple of months ago, resulting in the transfer. Thus far, I find the Schwab interface less intuitive than that of TD Ameritrade. Over time however, I hope to acclimate. Ultimately, the change is inconsequential, as I retain all of the same holdings and trade so infrequently that platform interface has minimal impact.

Transactions

SSNC- At the beginning of the quarter, I decided to liquidate my holdings in SSNC. While I continue to believe in the company’s strong fundamentals and future prospects, I have become increasingly concerned about its balance sheet. SSNC was once a much leaner Operation, a characteristic I found appealing, especially given the current higher interest rate environment. If interest rates remain elevated, the company’s debt load could become a more pressing issue. Additionally, growth has decelerated significantly. SSNC’s reliance on large acquisitions to drive revenue growth will add further debt in the future. Although I have no doubt that SSNC will continue to perform well, I believe reallocating my capital to other opportunities to be the best option going forward.

As always, I would like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Best way to reach me is on Twitter, follow me @TheGarpInvestor.