The first half of 2023 appeared bright and rosy, with soaring markets and unwavering investor confidence. My own stock portfolio saw impressive gains, and I felt like I was riding the crest of the investing wave. However, the third quarter unveiled the first cracks in this seemingly endless exuberance. While I’ve long foreseen a market correction, it seems my crystal ball is no match for Nostradomus; it took nearly three years for my prediction to materialize. Investors now find themselves rattled, and the prevailing sentiment has shifted to one of impending doom and gloom. As the adage goes, things are never quite as wonderful as they appear, but they are also never as dire as they may seem.

In the spirit of this investment blog, I’ll refrain from delving into global politics and the ongoing Middle East conflict. Suffice it to say, recent events have cast a heavy shadow, making the past week particularly challenging for me. Writing about seemingly inconsequential topics like investing becomes a tough endeavor when family and friends are living in the middle of a warzone.

Nevertheless, let’s refocus our attention on the matter at hand. The current market is under the influence of a rising interest rate environment. Rates impact on investments are akin to a gravitational pull, they change the entire framework. Assets that once seemed like bargains in a 3% interest rate scenario suddenly appear expensive when rates climb to over 7%. The question every investor must confront is whether it’s worth the risk to invest in stocks when they can purchase treasuries yielding over 5% at the moment.

It is evident that some stocks have taken a substantial hit, while others have demonstrated remarkable resilience. Notably, small and micro-cap stocks appear to be bearing the brunt of this downturn, whereas large and mega-cap equities have held their ground. Perhaps there is wisdom in considering a shift from the latter to the former, although personally, I won’t be making such changes. There is however certainly merit to considering a rebalancing strategy.

Today, we find ourselves at an intriguing juncture in time. The Federal Reserve’s efforts to quell inflation seem to be having an effect, but perhaps it is working a little too well. Companies are reporting relatively weak quarterly results, with falling revenues and earnings becoming all too common. Yet, I’ve never been more convinced that investing in outstanding companies offers the best defense in such circumstances. Owning businesses that can leverage a downturn to expand their market share, utilize their cash reserves to buy back shares, and take advantage of lower valuations by acquiring other companies represents a sound investment strategy.

As we navigate the current landscape, it is important to remember that the stock market is a long term proposition. Short term volatility, driven by shifting interest rates and economic uncertainties, is par for the course. While some investors may be tempted to jump ship and seek refuge in seemingly safer investments, it’s worth keeping in mind the wisdom of legendary investor Benjamin Graham. In the short run, the market is a voting machine, but in the long run, it is a weighing machine. In other words, fundamentals ultimately drive stock prices, and patient investors who stick with great companies during challenging times tend to reap the greatest rewards.

Q3 Performance

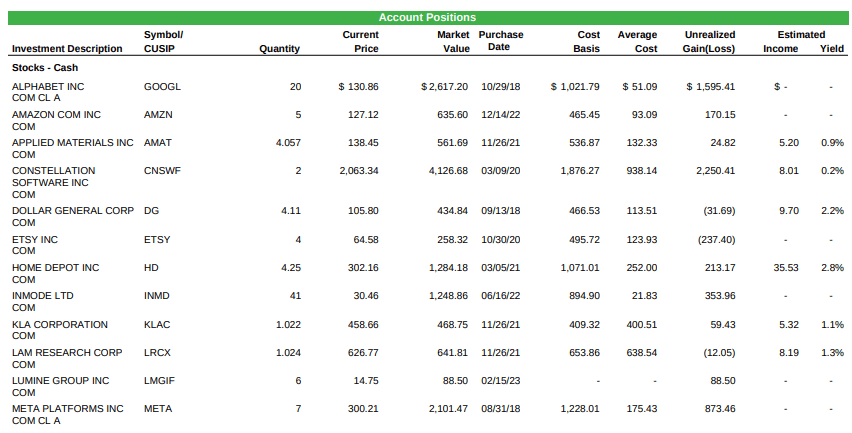

As of 10/1/2023, my 10K portfolio was worth $17,800.14. When I started on 8/19/18, the SPY had a price of $285.06 and my account started with $10,000. As of 10/1/2023 the SPY had a price of $427.48. In reality, the SPY has done even better due to dividends given out, so I have accounted for dividend reinvestment in the return calculation

| 10K Return(1) | SPY Return(2) | Difference(1-2) | |

| 2018(8/19-12/31) | (13.95) | (13.71) | (.24) |

| 2019 | 37.33 | 32.6 | 4.73 |

| 2020 | 21.22 | 17.59 | 3.63 |

| 2021 | 38.55 | 28.43 | 10.12 |

| 2022 | (27.25) | (18.65) | (8.60) |

| 2023(1/1-9/30) | 23.44 | 13.51 | 9.93 |

| Since Inception(8/19/18) | 78.00 | 63.52 | 14.48 |

| CAGR | 13.59 | 10.10 | 2.21 |

Despite my somewhat disheartened tone earlier, 2023 has in fact, been a remarkably successful year for my portfolio. Year to date, I’ve seen gains of over 23%. Admittedly, I may have lost a bit of my lead over the SPY, but I can hardly voice complaints when I still lead by 9.93% this year and 14.48% since inception. After five years in this experiment, I can at least acknowledge that I’ve demonstrated a modest degree of proficiency as an investor. I’ve managed to keep my financial shirt and have steered clear of any truly ill advised forays, like meme stocks or massive uses of leverage.

Nonetheless, five years remains a relatively brief time frame for making a substantial assessment. Genuine compounding, akin to the growth of a mighty oak from a humble acorn, requires the patience of a lifetime. The greatest rewards take decades to manifest. If I can simply maintain an annual outperformance of just a couple of percentage points, it will ultimately lead to a remarkable accumulation of wealth over the long haul.

Once again, I can declare that I refrained from making a single trade within my portfolio throughout the quarter. That very well might change this upcoming quarter however. Market turbulence can usher in promising opportunities. Thus, it should come as no surprise if I opt to make some transactions during the final quarter of 2023.

As always, I would like to thank you for taking the time to give this a read! Feel free to leave some comments or questions. Best way to reach me is on Twitter, follow me @TheGarpInvestor.